03 Jun 2026 Beijing Auto Show: Smart EVs are Scaled — and the Industry Moves Toward Intelligent Mobility

by Bill Russo

May 4, 2026

Introduction

Auto China 2026 confirmed what has been building for several years: China’s auto industry is no longer simply leading the transition to electrification. It is now setting the pace for the next competitive era — intelligent, connected, ecosystem-driven mobility.

The Beijing show did not feel like a traditional auto show. It felt more like a technology exhibition where the vehicle is becoming the delivery device for software, AI, energy infrastructure, intelligent cabins, autonomous-driving capability, and connected lifestyle ecosystems. The center of gravity has shifted. The question is no longer whether electric vehicles can scale. In China, they already have. The more important question is: who controls the intelligent mobility platform that sits on top of electrification?

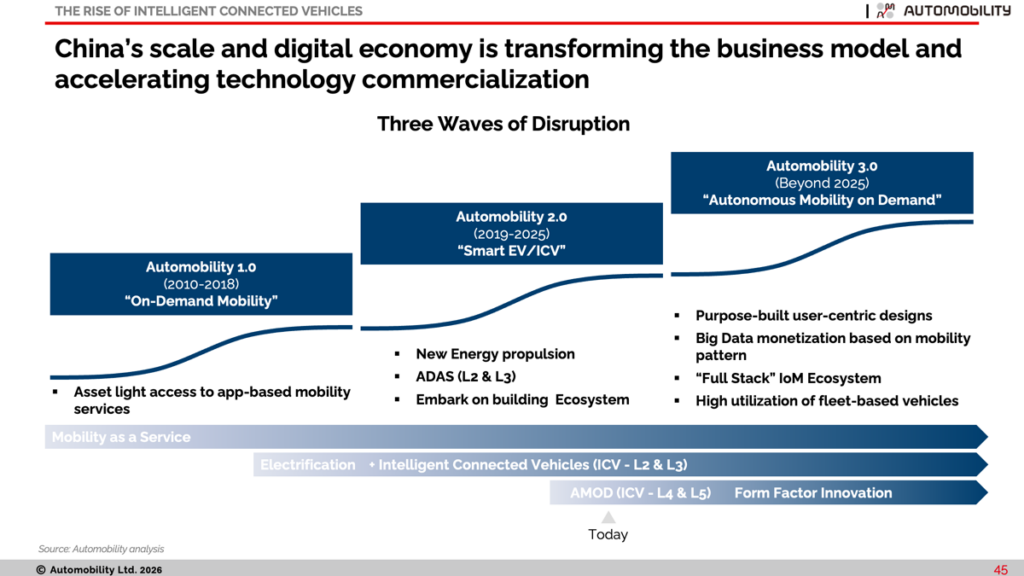

The best way to understand this transition is through Automobility’s three waves of disruption framework. Wave 1, Automobility 1.0, was the rise of on-demand mobility from 2010 to 2018, when app-based platforms changed how consumers accessed transportation without necessarily owning the asset. Wave 2, Automobility 2.0, from 2019 to 2025, has been defined by the scaling of Smart EVs and intelligent connected vehicles, combining new energy propulsion, L2/L3 assisted driving, connected cockpits, and the early construction of mobility ecosystems. Wave 3, Automobility 3.0, which begins beyond 2025, points toward autonomous mobility on demand, where purpose-built vehicles, full-stack Internet of Mobility ecosystems, big-data monetization, and high-utilization fleet models reshape the business model itself. Auto China 2026 matters because it showed that China is no longer merely participating in these waves — it is compressing them, scaling Wave 2 while already revealing the architecture of Wave 3.

Automobility’s Three Waves of Disruption Framework

Auto China 2026 provided clear evidence that the Smart EV era — what we call Wave 2 — has reached industrial scale. High-voltage EV platforms, L2+ advanced driver assistance systems, intelligent cockpits, over-the-air updates, and integrated digital services are no longer reserved for experimental flagships. They are becoming expected features across mainstream and premium segments. At the same time, the show offered early signs of Wave 3: the movement from smart electric vehicles as standalone products toward AI-defined, ecosystem-integrated mobility platforms.

This shift has major implications. Value is migrating from hardware alone to the integration of vehicle, software, energy, data, user experience, and ecosystem. Chinese companies are moving faster because they are operating in the world’s most competitive EV market, where rapid iteration is not optional. Global automakers, meanwhile, are being forced to localize, partner, and rethink long-standing assumptions about technology control.

Smart EV Wave 2 Is Fully Scaled

The first major takeaway from Auto China 2026 is that the Smart EV has become the new baseline. The industry has moved well beyond the early phase of electrification, when range, battery cost, and basic EV adoption were the primary concerns. In China, a competitive EV is now expected to deliver high-voltage charging, intelligent cockpit functions, advanced driver assistance, seamless connectivity, and fast software iteration.

The proof was everywhere on the show floor. BYD has pushed the industry toward high-voltage architecture and ultrafast charging, positioning charging speed as a mass-market competitive weapon rather than a niche technical achievement. NIO also demonstrated how premium EV brands are building around system-level capability rather than isolated vehicle features, combining intelligent vehicles with charging, swapping, and digital user services. XPENG showed the same pattern from a software-first angle, emphasizing full-stack development of ADAS, intelligent operating systems, and electronic/electrical architecture. Xiaomi reinforced that the car can be part of a larger “human-car-home” ecosystem, with the smart cabin connected to phones, devices, and digital services.

High Voltage Platform and Charging Innovation

Proofpoints: BYD and NIO showcasing 900V–1000V-class systems and ultrafast charging architectures; XPENG scaling urban and highway NOA capabilities through full-stack ADAS development; Xiaomi demonstrating that the smart cabin is now part of a broader consumer electronics ecosystem.

The implication is clear: Smart EV capability has moved from differentiation to table stakes.

Early Signs of Wave 3 Are Emerging

If Wave 2 was about making the EV smart, Wave 3 is about making mobility intelligent, adaptive, and ecosystem-driven. Vehicles are beginning to evolve from products into platforms — platforms that learn, update, connect, personalize, and integrate into broader digital ecosystems.

This is where the Beijing show was most revealing. XPENG’s messaging around AI mobility shows how automakers are beginning to define themselves beyond the vehicle. Its display included not only vehicles but also adjacent mobility technologies, signaling a broader ambition around embodied AI and future mobility systems.

Huawei’s HIMA ecosystem represents another version of this shift. Huawei is not a traditional automaker, but it is increasingly central to the intelligent vehicle value chain through cockpit systems, ADAS, connectivity, and brand partnerships. Its role across multiple OEMs suggests that future differentiation may come less from the OEM badge and more from the technology stack embedded inside the vehicle.

Xiaomi represents a third model. It approaches the car not as a standalone mobility product but as an extension of the user’s digital life. The vehicle becomes another node in a connected ecosystem that already includes smartphones, wearables, appliances, smart speakers, and home devices. That matters because consumer expectations are being shaped less by traditional automotive benchmarks and more by the speed, convenience, and personalization of consumer technology.

XPENG’s IRON Humanoid Robot [Photo: Bill Russo]

Proof points: XPENG positioning itself around AI-defined mobility rather than simply EV manufacturing; Huawei expanding HIMA across multiple OEM partners and vehicle segments; Xiaomi integrating the vehicle into its HyperOS-powered human-car-home ecosystem.

Wave 3 is not yet fully formed. But the direction is visible: the vehicle is becoming an intelligent interface between people, mobility, energy, and digital life.

Electrification Is Now Infrastructure

Another important lesson from Beijing is that electrification is no longer just about putting batteries into vehicles. It is becoming infrastructure. The competitive focus is shifting from whether a vehicle is electric to how quickly, efficiently, and conveniently it can replenish energy.

In mature EV markets, charging speed and infrastructure availability become central to consumer confidence. China is now attacking this problem with both technological and business-model innovation. BYD is pushing flash-charging and high-voltage architectures. NIO continues to expand battery swapping. Battery suppliers are racing to reduce charge times and improve high-power performance. The direction is clear: the industry is trying to move the EV ownership experience closer to — and eventually beyond — the convenience of gasoline refueling.

This is strategically important. Once EV charging becomes fast enough, dense enough, and reliable enough, the psychological advantage of gasoline refueling starts to erode. That changes not only consumer adoption but also the competitive basis of the industry. Energy replenishment becomes part of the platform experience.

BYD’s Low Temperature Flash Charging [Photo: Bill Russo]

Proof points: BYD flash-charging and 1000V architecture targeting refueling-like convenience; NIO battery swapping expanding the definition of EV infrastructure beyond charging piles; premium and joint-venture brands aligning around 800V–900V-class platforms and faster charging.

Electrification has crossed an important threshold. The race is no longer only about batteries inside vehicles. It is about energy systems around vehicles.

Chinese Brands Are Redefining Premium

Auto China 2026 also showed that Chinese brands are no longer content to compete from below. They are moving directly into premium segments and redefining what premium means.

Historically, premium in China was associated with foreign badges, mechanical refinement, heritage, and status. That definition is changing. Increasingly, premium is being defined by technology density, interior space, intelligent driving, digital experience, charging capability, and ecosystem integration.

NIO’s ES9 is a strong example. Rather than relying on traditional luxury cues alone, NIO positioned the ES9 around executive space, smart electric architecture, full-stack technologies, and a flagship user experience. Li Auto has also helped reshape the premium family SUV category by focusing on space, comfort, range confidence, family use cases, and intelligent cockpit experience. Luxeed’s V9 entry into the premium MPV segment under the Huawei-backed ecosystem points to the same trend: technology ecosystems are now moving into high-value family and executive mobility categories

Li Auto L9 [Photo: Bill Russo]

Proof points: NIO ES9 reinforcing Chinese-brand credibility above RMB 500,000; Li Auto’s L9 family SUV success showing that premium can be defined by use-case experience, not only badge heritage; Luxeed V9 pushing Huawei’s ecosystem logic into the premium MPV segment.

The deeper point is that Chinese brands are not merely catching up in premium. They are changing the criteria by which premium is judge

Global OEMs Are Adapting Through Localization and Partnerships

For global automakers, Auto China 2026 was a reality check. China remains too important to exit, but too fast-moving to approach with legacy global playbooks. The result is a visible shift toward local partnerships, China-specific architectures, and external technology adoption.

Volkswagen’s cooperation with XPENG is one of the clearest examples of this adaptation. Rather than relying only on global platforms developed outside China, VW is using a Chinese partner to accelerate product development and improve local technology relevance. Audi’s work with SAIC follows a similar logic, combining a global premium brand with a China-developed digital and EV architecture. Toyota’s adoption of Huawei and Momenta technologies in China shows that even the most globally disciplined automakers are adapting to local intelligent-vehicle ecosystems.

JV and Premium Brands are Leveraging Local Partnerships

Proof points: Volkswagen-XPENG integration showing partnership-driven product acceleration; Toyota using Huawei and Momenta technology in China-market EVs; Audi developing China-exclusive EVs with SAIC and localized digital architecture.

The lesson is blunt: in China, global OEMs must trade some control for speed and relevance.

Ecosystem Players Are Becoming Central

Perhaps the most important structural shift is that value is moving from OEMs alone to platform and ecosystem players. Huawei, Xiaomi, Momenta, CATL, BYD’s battery and charging systems, and other technology providers are increasingly shaping the consumer experience and competitive boundaries of the industry.

Huawei is the most visible example because it can influence multiple brands without becoming a conventional automaker. Through HIMA and its technology stack, Huawei can shape cockpit experience, intelligent driving, connectivity, and brand perception across different OEM partners.

Xiaomi is equally disruptive, but in a different way. Its advantage comes from consumer electronics, operating systems, devices, and user ecosystem. The vehicle is an extension of that ecosystem, which changes how customers evaluate convenience, personalization, and daily-life integration.

ADAS suppliers such as Momenta are also gaining influence as global and domestic OEMs look for faster paths to China-relevant intelligent-driving capability. This suggests that the automotive value chain is becoming more modular, more software-driven, and more dependent on ecosystem orchestration.

Uniform Exterior and Interior Design Across HIMA Brands Hightlights Huawei’s Dominance

Proof points: Huawei appearing across multiple brands and vehicle categories; Xiaomi turning the vehicle into part of a broader connected lifestyle; ADAS suppliers gaining strategic influence as OEMs race to localize intelligent-driving features.

The center of value is shifting. The OEM still matters, but the platform increasingly defines the experience.

Competitive Gaps Are Widening

The final takeaway is that competitive gaps are widening. Leaders are scaling faster, while followers are increasingly dependent on partnerships to remain relevant.

This is not only about technology. It is about organizational speed. Chinese automakers operate in an environment where product cycles are shorter, software updates are expected, consumer feedback loops are faster, and competitive pressure is relentless. That forces faster iteration. It also rewards companies that can integrate hardware, software, energy, and user experience into a coherent system.

Global OEMs still have strengths: engineering depth, safety, manufacturing quality, global brands, and worldwide scale. But in China, those strengths are no longer sufficient by themselves. The market now rewards speed, localization, and digital ecosystem relevance.

China’s Leapfrog Resets the Rules of Competition

Proof points: Chinese OEMs iterating faster across EV platforms, ADAS, cockpit, and charging; joint ventures relying more heavily on Chinese partners for architecture, software, and ADAS; rapid product cycles widening the capability gap between leaders and slower-moving followers.

Auto China 2026 showed that the industry’s competitive battlefield has changed. Electrification is now the foundation. Intelligence is the battleground. Ecosystems are the multiplier. Speed is the weapon.

Conclusion: From Electrification to Intelligence

Auto China 2026 confirmed the transition from the EV era to the intelligent mobility era. Smart EVs are now scaled. High-voltage platforms, AI cockpits, L2+ ADAS, fast charging, and software-defined features are becoming normal. The next frontier is integration: vehicles connected to energy systems, digital ecosystems, AI agents, smart homes, and mobility services.

China is setting the pace because its market compresses the future. Competition is intense, consumers are demanding, infrastructure is advancing, and technology companies are deeply embedded in the mobility value chain.

The message from Beijing is clear: the future of the auto industry will not be won by electrification alone. It will be won by those who can integrate intelligence, ecosystem, infrastructure, and speed into a compelling mobility experience.

About the Author

Bill Russo is the Founder and CEO of Automobility Ltd , and is currently serving as the Chairman of the Automotive Committee at the American Chamber of Commerce in Shanghai. His over 40 years of experience includes 15 years as an automotive executive with Chrysler, including 21 years of experience in China and Asia. He has also worked nearly 12 years in the electronics and information technology industries with IBM and Harman. He has worked as an advisor and consultant for numerous multinational and local Chinese firms in the formulation and implementation of their global market and product strategies. Bill is a contributing author to the book Selling to China: Stories of Success, Failure, and Constant Change (2023), where he describes how China has become the most commercially innovative place to do business in the world’s auto industry – and why those hoping to compete globally must continue to be in the market.

Contact Bill by email at bill.russo@automobility.io

About Automobility

Automobility Limited is global Strategy & Investment Advisory firm based in Shanghai that is focused on helping its clients to Build and Profit from the Future of Mobility. We help our clients address and solve their toughest business and management issues that arise in midst of fast changing, complicated and ambiguous operating environment. We commit to helping our clients to not only “design” the solutions but also raise or deploy capital and assist in implementation, often together with our clients.

Contact us by email at info@automobility.io

Sorry, the comment form is closed at this time.