26 Apr State of China’s Auto Market – April 2026

Written by Bill Russo, Founder & CEO of Automobility Ltd.

Before we dive into the market results in China for the 1st quarter, it’s important to recognize that the current Middle East conflict is not just a geopolitical event—it is a structural inflection point for the automotive industry. Much like the energy shocks of the 1970s reshaped consumer behavior and accelerated a shift toward fuel efficiency, today’s disruption is likely to reframe how consumers think about energy risk, operating cost, and mobility choice.

Rising fuel volatility does more than pressure demand in the near term—it reinforces the economic logic of electrification, accelerating the shift toward vehicles that decouple from oil dependence. In that sense, this crisis is not only a headwind for the industry—it is also a catalyst that will shape consumer preferences, competitive positioning, and the pace of transition for years to come.

I explore these structural implications in more detail in this article:

The Impact of the Current Middle East War on the Global Automotive Industry

Key Headlines Summary through 1st Quarter 2026

📉 China auto demand remains under pressure, with 1Q sales down ~20% YoY as March recovery fails to offset a weak start and exposes underlying consumption softness.

⚡ Electrification holds scale but loses momentum, with NEV share stabilizing ~42–43%—below Q4 peaks—as both mix and volumes reflect softer demand.

🎯 Policy normalization is biting harder than expected, revealing high price sensitivity in mass-market EV segments rather than just seasonal distortion.

🌍 Exports have become the structural stabilizer, sustaining ~30%+ share even after February’s spike, anchoring industry volume amid domestic weakness.

🚀 China’s global expansion continues to deepen, with export growth broadening geographically and NEVs approaching ~43% of export mix.

🔄 Competition is intensifying in a no-growth environment, shifting from expansion-driven to share-shift dynamics across both ICE and NEV segments.

🧠 Smart EV disruption is accelerating but volatile, with tech-led players (Xiaomi, HIMA, Li Auto) gaining ground amid uneven monthly demand swings.

🏭 The industry is structurally transitioning to an export-anchored, overcapacity-driven system, where global markets—not domestic growth—absorb incremental output.

China Auto Market 1Q 2026: Domestic Weakness Forces a Strategic Pivot to Global Markets

China’s auto market entered 2026 under clear pressure, with first-quarter sales down roughly 20% year-over-year as a weak January–February was only partially offset by a March rebound. What initially appeared to be seasonal distortion is now revealing something more fundamental: underlying consumption softness. At the same time, electrification—while still firmly scaled—has lost some near-term momentum, with NEV penetration stabilizing in the low-40% range, below late-2025 peaks. Policy normalization is proving more disruptive than expected, exposing high price sensitivity in mass-market EV segments and dampening both volume and mix.

In response, the industry is executing a decisive pivot outward. Exports have become both a safety valve and a margin lever—absorbing excess capacity while offering access to higher-priced markets and stronger pricing discipline than China’s hyper-competitive domestic arena. This dual role is reshaping the industry’s structure: global markets are no longer incremental—they are essential. As export share sustains above 30% and NEVs approach half of outbound volume, China’s auto sector is evolving into an export-anchored system where profitability, not just volume, is increasingly determined overseas. In a no-growth domestic environment, competition intensifies, smart EV disruptors gain ground, and the center of gravity continues to shift toward those able to scale globally with differentiated, higher-value products.

China Auto Demand Moderates as Policy Support Rolls Off

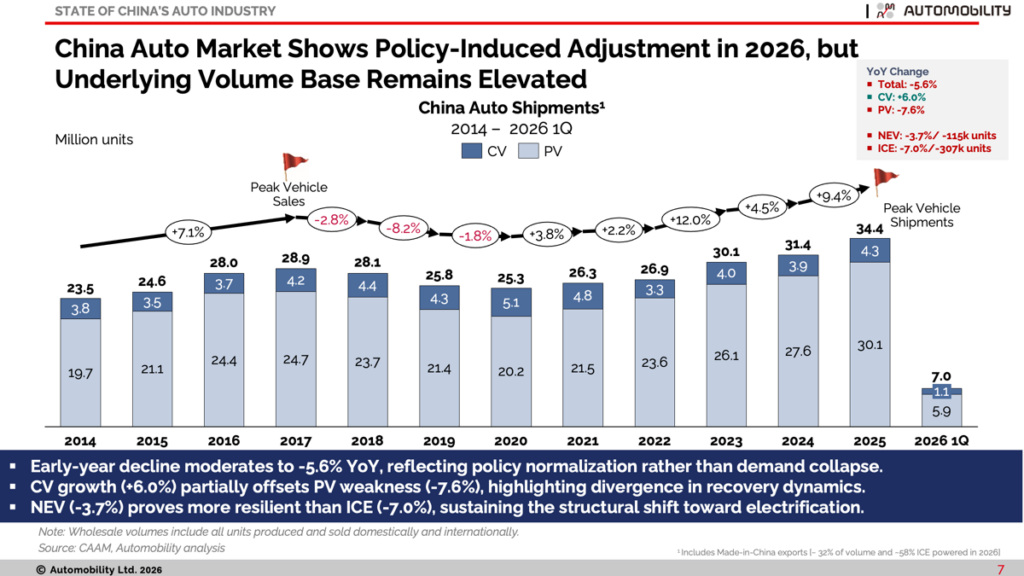

China’s auto industry entered 2026 from a record year in 2025, when total vehicle shipments reached ~34.4 million units, up ~9.4% YoY and surpassing the prior peak in 2017. This confirms the industry is operating at a new structural scale, increasingly supported not only by domestic demand but also by a rising contribution from exports, which now represent roughly one-third of total volume.

The first quarter of 2026 reflects a policy-driven adjustment, with shipments declining ~5.6% YoY. This moderation is less severe than early-year monthly volatility suggested and is primarily driven by policy normalization, Lunar New Year timing, and payback from the incentive-driven surge in late 2025. However, beneath this normalization, passenger vehicle demand remains soft, while commercial vehicles provide a partial offset, highlighting a divergence in recovery dynamics.

Electrification continues to anchor the industry’s structural shift. In 2025, NEV shipments expanded strongly, reinforcing their role as the primary growth engine. In 1Q 2026, NEV volumes declined modestly (–3.7% YoY), but remained more resilient than ICE, which contracted more sharply (–7.0%). This gap underscores that electrification is still gaining share even in a weaker market environment, though momentum has moderated following the late-2025 peak.

Overall, the data reinforces a rebalanced operating model for China’s auto industry: growth is no longer driven purely by domestic expansion. Instead, exports underpin scale, electrification reshapes the mix, and policy shifts increasingly influence near-term volatility. The early-2026 slowdown reflects normalization within this new structure—not a reversal of the elevated baseline established in 2025.

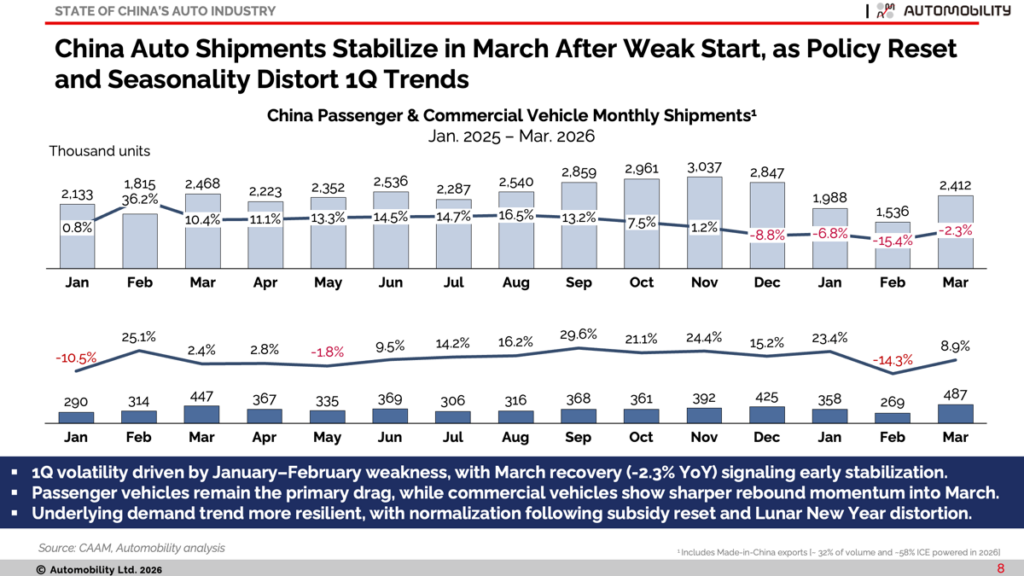

Shipments slowed sharply at the start of 2026, with passenger vehicle volumes falling to ~2.0 million units in January and further to ~1.54 million units in February (–6.8% and –15.4% YoY). This early weakness reflects policy normalization and Lunar New Year timing, following the pull-forward of demand into late 2025.

March shows a partial recovery, with volumes rebounding to ~2.41 million units (–2.3% YoY), indicating early stabilization but not a full return to prior-year levels. Passenger vehicles remain the primary drag, while commercial vehicles demonstrate stronger rebound momentum. Overall, the pattern suggests normalization with underlying softness, rather than a clean seasonal reset or a sharp demand shock.

The opening months of 2026 illustrate a market transitioning from incentive-driven strength to a more normalized—and weaker—demand environment. While policy roll-offs and Lunar New Year timing explain much of the early volatility, the incomplete recovery in March suggests softness extends beyond seasonal effects. Passenger vehicles remain the primary source of weakness, while commercial vehicles provide only a partial offset.

Overall, the data points to more than just normalization. Policy reset is exposing underlying demand fragility, particularly in price-sensitive segments, even as the industry remains structurally supported by electrification and exports. The result is a market that is stabilizing sequentially, but at a lower underlying demand level than 2025 peaks, indicating a shift from policy-driven expansion to a more constrained growth phase.

From Volume Overflow to Profit Engine: Exports Redefine China’s Auto Industry Model

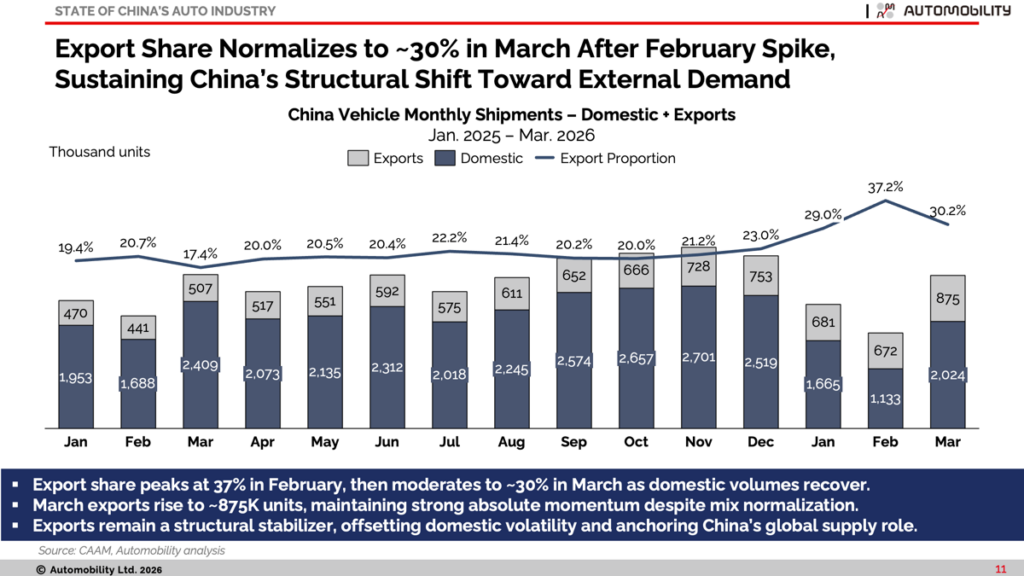

China closed 2025 with a record ~7.1 million vehicle exports, marking a clear transition from exports as a pressure release valve to a core engine of both scale and profitability. That shift has become more pronounced in 1Q 2026. As domestic demand weakens, exports are not just absorbing excess capacity—they are increasingly supporting pricing discipline and improving average selling prices, offering access to less saturated and higher-margin markets than China’s intensely competitive home base.

The first quarter underscores how structurally embedded this shift has become. Export share spiked to ~37% in February as domestic demand softened, then normalized to ~30% in March as volumes partially recovered—yet remained elevated by historical standards. Importantly, March Made-in-China exports reached a new record high in absolute terms, reinforcing the strength of external demand even as mix dynamics normalized. This highlights a system that is no longer domestically anchored. Instead, China’s auto industry is evolving into a globally balanced operating model, where exports flex to stabilize volume while simultaneously enhancing value realization, reinforcing their dual role as both safety valve and profit lever.

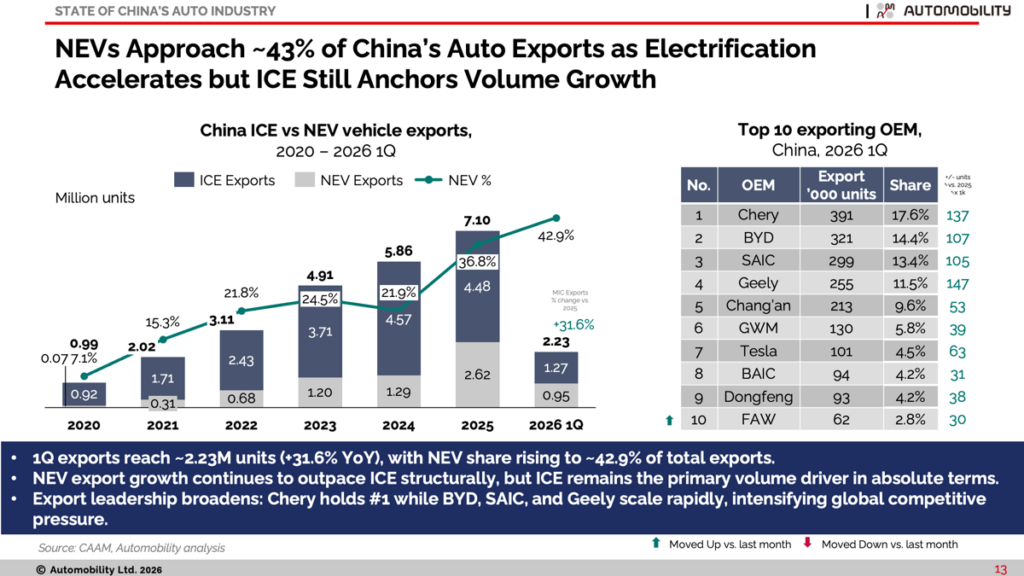

Exports have extended their role beyond cyclical support to become a primary driver of industry scale and competitive positioning. In 1Q 2026, shipments reached ~2.23 million units (+31.6% YoY), reinforcing the growing dependence on overseas markets as domestic demand softens. Increasingly, exports are not just absorbing excess capacity—they are setting the pace for growth, utilization, and pricing discipline across the industry.

At the same time, the export mix is shifting structurally toward electrification. NEVs now account for ~43% of total exports, signaling a transition from ICE-led volume expansion to EV-driven competitive advantage. While ICE continues to anchor absolute volume, NEVs are shaping margins, brand positioning, and long-term global share. Export leadership is also broadening, with Chery maintaining the top position while BYD, SAIC, and Geely scale rapidly—intensifying competition as Chinese OEMs deepen their global footprint.

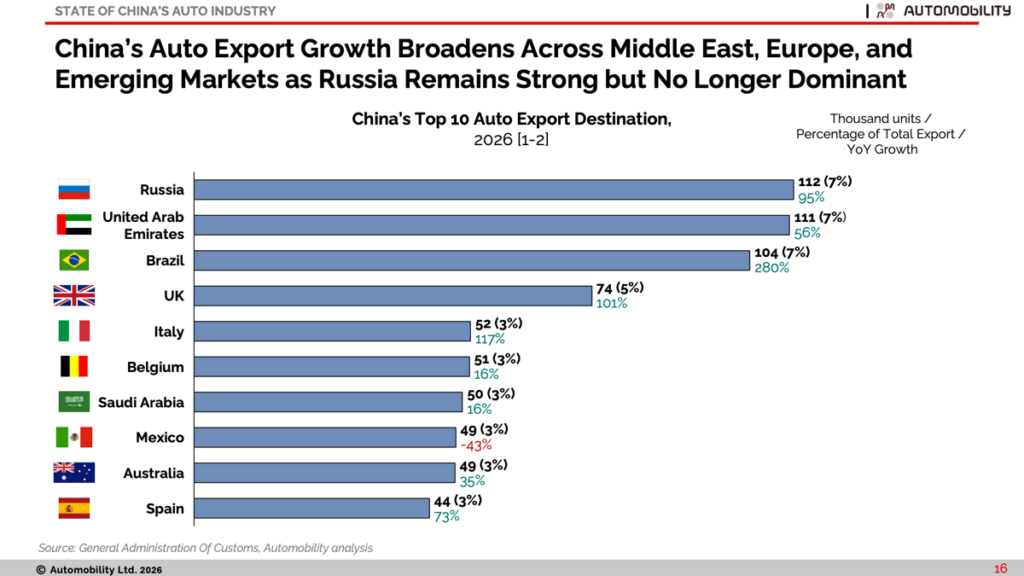

China’s export growth is broadening across regions and becoming less concentrated, reflecting a more diversified global footprint. In early 2026, strong momentum is evident across the Middle East, Europe, and emerging markets, with the UAE, Brazil, and key European destinations showing robust growth. This shift underscores expanding demand beyond traditional markets and highlights the increasing importance of multi-regional demand drivers in sustaining China’s export engine.

At the same time, Russia’s role is evolving. While volumes remain significant in early 2026, its relative dominance has diminished as growth accelerates elsewhere. The contrast reflects how China’s export trajectory is increasingly shaped not just by demand, but by policy, regulatory environments, and market accessibility. This is also evident in Mexico, where volumes have declined—likely reflecting rising policy friction and trade uncertainty, including tariff risks and local industrial policy dynamics that are beginning to constrain growth. As Chinese OEMs scale globally, export growth is becoming more balanced—and more complex—driven by a wider set of geopolitical and economic factors rather than reliance on any single anchor market.

China’s Market Peaked in 2017—Profit Growth Shifts to Mix, Not Volume

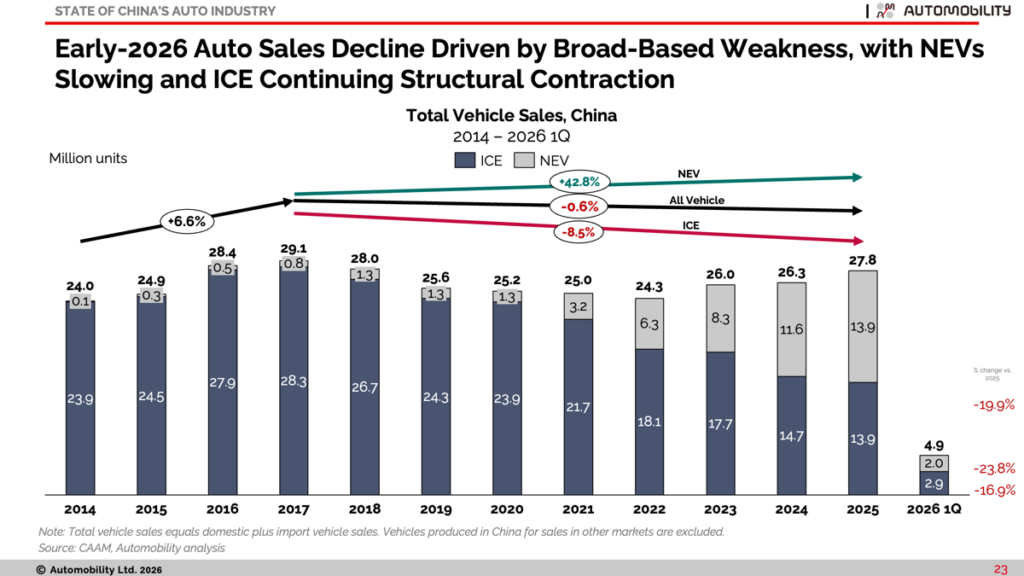

China’s domestic auto market has clearly moved into a new phase. After a strong 2025, early-2026 sales have weakened materially, with 1Q volumes down ~20% YoY—highlighting that the era of volume-driven growth has ended. This slowdown is broad-based, affecting both ICE and NEV segments, with electrification still expanding structurally but no longer able to fully offset cyclical demand softness. The result is a market where total demand is under pressure even as the transition continues.

What has not changed is the direction of travel. All structural growth still comes from electrification, while ICE continues its steady decline. But the key shift is that NEVs are no longer a growth engine on top of a rising market—they are now carrying the market within a constrained demand environment. Domestic demand is stabilizing at a lower baseline, and the industry’s operating model is adjusting accordingly, with exports increasingly required to sustain scale and absorb excess capacity.

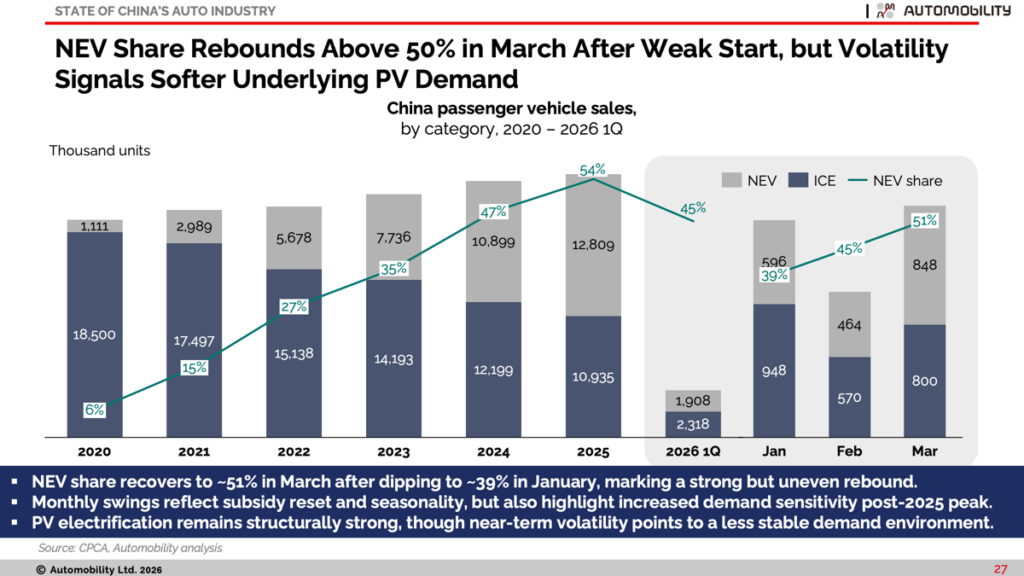

The late-2025 inflection point remains intact, but early 2026 reveals a more volatile and demand-sensitive phase of electrification. NEV share, which peaked above 50% in Q4, dropped sharply to ~39% in January before rebounding to ~51% in March. This confirms that the market has structurally crossed over—but also that the pace of that transition is no longer linear.

What is becoming clear is that NEVs are now operating within a constrained demand environment, not simply expanding within a growing market. While they continue to outpace ICE structurally, both mix and volume fluctuations point to heightened sensitivity to policy changes, pricing, and consumer confidence. The gap between NEV and ICE remains decisive, but near-term dynamics suggest a market that is stabilizing at a higher electrification level, with more volatility and less momentum than in the incentive-driven phase of 2025.

From Dominance to Dogfight: China’s NEV Market Enters Its Most Competitive Phase Yet

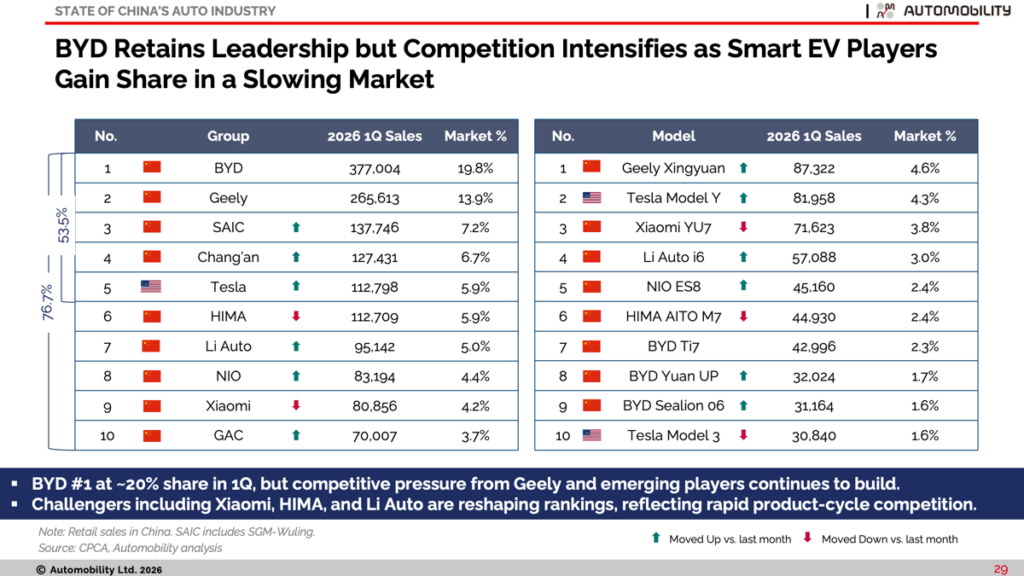

Early-2026 confirms that BYD remains the clear leader, but the nature of that leadership is changing. In a slowing market, share gains are no longer driven by expansion but by intensifying competition for limited incremental demand. Geely has solidified its #2 position, while Tesla, HIMA, and other players are clustering closely behind—highlighting a market that is tightening rather than spreading.

What stands out is the rapid rise of smart EV challengers, with Xiaomi, HIMA, and Li Auto reshaping both group and model rankings. At the nameplate level, leadership is increasingly defined by technology, software integration, and ecosystem strength, not just scale. The result is a structural shift from a dominant-leader model to a high-velocity competitive environment, where positioning can change quickly and differentiation—not volume alone—determines momentum.

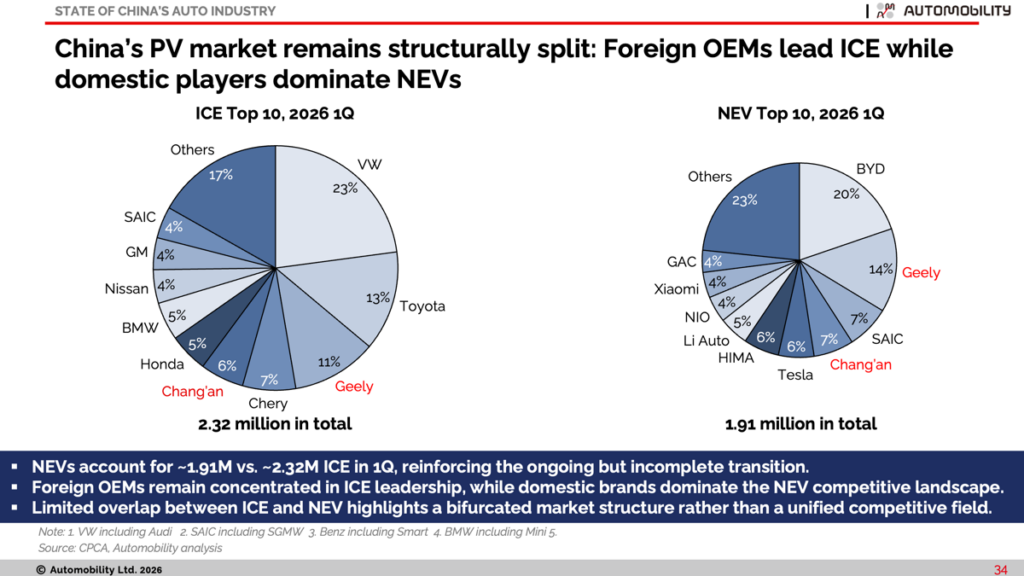

China’s passenger vehicle market has not just crossed over to NEVs—it is now entering a phase where policy sensitivity is actively reshaping competitive outcomes. Early-2026 results show that demand is no longer uniformly rising with electrification; instead, it is becoming more selective, price-aware, and uneven across segments. The rollback of incentives has exposed where underlying demand is truly durable—and where it was artificially supported.

What emerges is not just bifurcation, but segmentation under pressure. ICE and NEV are no longer simply two competing powertrains—they represent different competitive ecosystems with limited overlap. Foreign OEMs remain anchored in a shrinking but still defensible ICE space, while domestic players dominate NEVs but face increasing volatility within that domain. The real divide is not ICE vs. NEV—it is resilience vs. sensitivity. OEMs with diversified portfolios and scale can absorb policy shocks, while narrower, subsidy-dependent players are now being tested in a market that is transitioning from policy-driven growth to market-driven selection.

BYD remains China’s NEV leader, but the latest data highlights that leadership is now being contested within a structurally fragmented market, rather than challenged by a single rival. The dynamics shaping share are less about strategy shifts and more about how the market itself is evolving.

-

The competitive battlefield has narrowed and intensified within NEVs, as ICE and NEV ecosystems diverge further. With limited overlap between the two, BYD is no longer competing with legacy incumbents—it is competing in a high-density cluster of domestic NEV specialists. -

Share is being redistributed, not displaced. The rise of Geely, HIMA, SAIC, and others reflects a broadening of credible competitors rather than a zero-sum shift away from BYD. This creates continuous share churn at the top, even as overall leadership remains intact. -

Demand is becoming more segmented by value and technology, with different players winning in different price bands and use cases. This reduces the ability of any single OEM to dominate across the full spectrum, leading to natural dilution of share even in a growing category. -

Market leadership is becoming more dynamic and model-driven, not just brand-driven. Rapid product cycles, frequent launches, and shifting consumer preferences mean that short-term ranking volatility is now a structural feature, not an anomaly.

In this context, BYD’s share variability reflects a transition from category creation to category competition. The company remains the benchmark player, but the market it helped build is now large, diverse, and competitive enough that leadership no longer implies concentration.

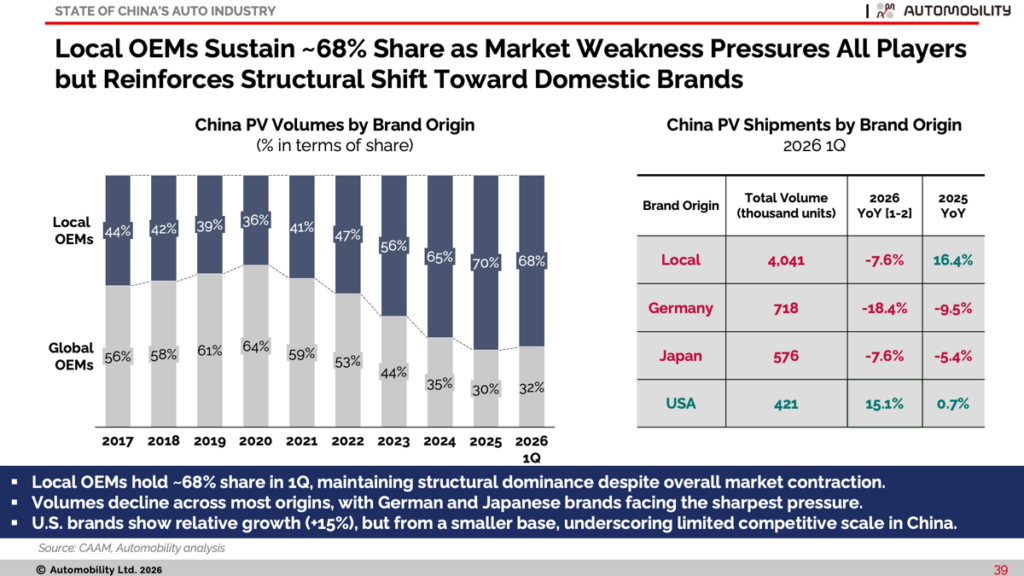

Domestic Brands Hold the Line as Market Weakness Tests Global Competitors More Severely

China’s passenger vehicle market in early 2026 is revealing a stress test of competitive positioning rather than a shift in leadership. Local OEMs continue to hold ~68% share, not because the market is expanding, but because they are proving more resilient in a contracting environment. While volumes have declined across all major brand origins, the sharper pullback among German and Japanese OEMs highlights their greater exposure to weakening ICE demand and slower adaptation to shifting consumer preferences.

What stands out this quarter is not just dominance, but relative defensiveness. Domestic players are better aligned with current demand conditions—particularly in electrification and value-oriented segments—allowing them to protect share even as absolute volumes fall. By contrast, global OEMs are being squeezed between declining ICE relevance and still-limited competitiveness in NEVs. U.S. brands show pockets of growth, but from a small base, reinforcing that the competitive gap is structural, not cyclical. The result is a market where contraction is not redistributing leadership—it is reinforcing it.

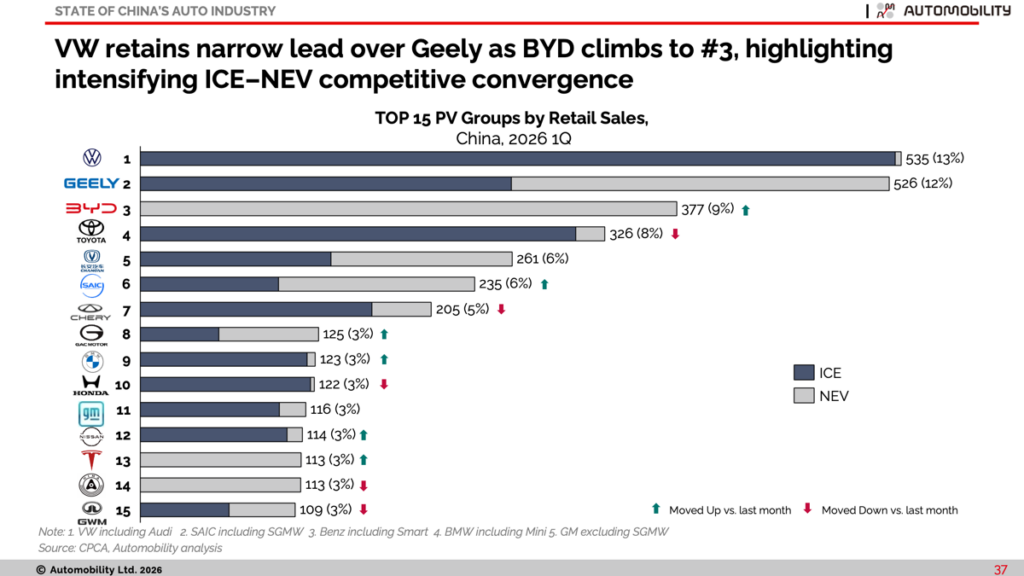

The 1Q 2026 rankings reflect a compression at the top rather than a simple reshuffle, with VW narrowly retaining the lead over Geely while BYD climbs to #3—highlighting how competition is intensifying across both ICE and NEV domains. The key movement is not just positional change, but the narrowing gap between fundamentally different business models, as ICE incumbents and NEV leaders increasingly compete within overlapping demand pools.

What stands out is the divergence in how players are moving. Geely’s strength comes from balance across ICE and NEV portfolios, allowing it to remain consistently competitive, while BYD’s rise reflects scale in electrification despite a softer domestic demand environment. Meanwhile, Toyota’s relative decline underscores the growing difficulty for ICE-heavy players to defend position without meaningful NEV contribution.

More broadly, the rankings signal a transition from a segmented market to one defined by convergence and cross-powertrain competition, where leadership is no longer determined by dominance in a single category, but by the ability to compete across both. This is creating tighter clustering at the top and more fluid movement between ranks, as product mix, pricing, and demand volatility increasingly drive short-term positioning.

Conclusion: A Weaker Market Reveals a Stronger Structural Shift

The first quarter of 2026 makes one thing clear: this is not just a normalization story—it is a stress test of the new industry model. The sharp early-year decline and only partial March recovery expose underlying demand softness, particularly in price-sensitive segments, as policy support fades. Electrification continues to define the direction of travel, but momentum has moderated, and the market is now operating under tighter, more demand-constrained conditions than in the incentive-driven phase of 2025.

At the same time, the structural shifts have become more visible—and more decisive. Exports have moved from a cyclical buffer to a core operating pillar, sustaining scale and increasingly supporting profitability. Competition has intensified in a no-growth environment, with share gains driven by product strength, technology differentiation, and global reach rather than policy tailwinds. The industry is no longer expanding uniformly—it is selecting winners.

Looking ahead, the key question is not whether the transition continues, but who benefits from it. As domestic demand stabilizes at a lower level and electrification enters a more competitive phase, execution—not policy—will determine outcomes. The winners will be those who can balance domestic resilience with global expansion, control key technologies, and compete effectively in a market where growth is harder to find—and easier to lose.

AmCham Shanghai State of China Auto Market Monthly Webinar [April 21]

Join us on Tuesday, April 21, from 9:00 am – 10:15 am China time for the monthly AmCham Shanghai State of China Auto Market Monthly Webinar, where we will review the latest market results through March 2026 and highlight recent news from the world’s largest and most progressive automotive market.

Webinar | State of China Auto Market Monthly Briefing (April) | AmCham Shanghai

Leadership Lessons: A Conversation with Bill Russo

On March 12, I was honored to be the featured guest at The American Chamber of Commerce in Shanghai (AmCham Shanghai) Future Leaders Committee event, where I reflected on and shared the journey that shaped my career and the leadership lessons learned along the way.

From my early days at Columbia Engineering, to semiconductor manufacturing at IBM, to strategy leadership at Daimler Chrysler, and eventually founding Automobility Ltd, one lesson stands out:

Leadership often comes down to recognizing inflection points — the moments when industries, technologies, and strategies fundamentally shift.

Today, the mobility industry is living through one of those moments.

Electrification, connectivity, software-defined vehicles, and AI are transforming the automobile from a mechanical product into a connected mobility platform. And increasingly, many of these shifts are unfolding at China speed.

In the talk, I share a few reflections for the next generation of leaders:

🔹 Don’t chase titles — chase inflection points

🔹 Build systems fluency across technology, policy, capital, and culture

🔹 Choose geography deliberately — where you stand determines what you see

🔹 Think in decades, not quarters

Careers compound the same way capital does: slowly… and then suddenly.

📺 Here is a short video prepared for the event:

We are pleased to share Episode 6 of the Auto Insider podcast—continuing our series of candid, in-depth conversations with leaders operating at the center of the global mobility reset.

In Episode 6 of Auto Insider, I sit down with Dr. Simon Yang, President of China and Asia Pacific at Aptiv, for a deeper examination of how the automotive value chain is being structurally reshaped in the era of intelligent mobility. This is not a surface-level discussion of electrification or software—it’s a grounded look at how architecture, integration, and speed are redefining competitive advantage.

We explore how Aptiv is repositioning itself from a traditional Tier-1 supplier to a system architecture partner, enabling OEMs to build software-defined vehicles that can scale across markets while keeping pace with China’s compressed development cycles. The conversation highlights the shift from component excellence to platform-level orchestration, where value increasingly sits in the ability to integrate hardware, software, and data into cohesive, upgradable systems.

At the center of this discussion is China’s transformation from fast follower to global innovation anchor. We unpack what “China for Global” really means in practice—not just exporting products, but exporting development models, speed, and ecosystem-driven innovation. That shift is forcing global players to rethink how they collaborate, localize, and compete.

We also address the uncomfortable reality: the traditional supplier model is under pressure. Success now depends on deeper integration with OEMs, closer alignment with local ecosystems, and the ability to operate at China speed without losing global scale discipline.

The takeaway is clear—this is a structural transition, not a cyclical one. The companies that win will be those that can architect systems, not just supply components, and translate China’s pace of innovation into globally scalable solutions.

🎙️ Catch up on the latest episodes of the Auto Insider Podcast hosted by Bill Russo, featuring insights from the front lines of China’s mobility transformation — where speed, scale, and strategy are redefining global competition.

🌏 Episode #5: Safety Without Borders: How Autoliv Drives Scaled Collaboration in the Smart Mobility Era with Sng Yih, President, Autoliv China

🌏 Episode #4: Leapmotor’s Global Leap — A New Paradigm for Global EV Collaboration with Michael Wu, Co-President, Leapmotor

🚗 Episode #3: Competing at China Speed: A Tier-1 Perspective from Magna with Zhen Wu, President of Magna China

🦋 Episode #2: The Butterfly Effect—How China’s Auto Shift is Reshaping the World with Dr. Xiaozhi Liu, Founder and CEO of ASL Automotive, Former CEO of Fuyao Glass

🔧 Episode #1: Smart EVs and the Smart Tier 0.5 Supply Chain with Jack Cheng , Co-Founder of NIO and CEO of M-Mobility

We’re just getting started — more conversations coming soon with the visionaries shaping the future of mobility.

FUTURE OF MOBILITY AUDIO INTERVIEW SERIES

To frame this shift, I participated in a three-part audio interview series with Ron Hesse from GlobalAutoIndustry.com that explores the Automobility 1.0–2.0–3.0 framework—from the move away from vehicle ownership toward usage-based mobility, through today’s connected, electric, and intelligent vehicle era, and ultimately toward autonomous, AI-driven mobility platforms.

Links to the three interviews—Automobility 1.0 to 3.0—are provided below:

Automobility 1.0: The Shift from Ownership to Usage – A China Perspective

Automobility 2.0: Connected, Electric & Intelligent – A China Perspective

Automobility 3.0: Autonomous & Distributed Mobility – A China Perspective

AUTOMOBILITY ARTICLES

BYD Is Losing Share in China — and That May Be Exactly the Point

Is BYD really losing ground in China — or pivoting a different game?

About Bill Russo

Bill is a contributing author to the book Selling to China: Stories of Success, Failure, and Constant Change (2023), where he describes how China has become the most commercially innovative place to do business in the world’s auto industry – and why those hoping to compete globally must continue to be in the market.

About Automobility

Contact us by email at info@automobility.io

PLEASE NOTE: The information and analysis shared in this newsletter, including the charts and style of materials presented, is the intellectual property of Automobility Ltd. While we share it as a way to serve our existing and new clients, it is not to be used without our express consent and then only with attribution. Any publication, reproduction or other use of this material without the express written consent of Automobility Ltd is prohibited.

Sorry, the comment form is closed at this time.