26 Apr The Impact of the Current Middle East War on the Global Automotive Industry

A Structural Analysis of Supply, Demand, Competitive Power, and the Shift in Industry Center of Gravity

by Bill Russo

April 5, 2026

Automobility analysis | Energy shock is reshaping the global auto industry, visualized with AI

Executive Perspective

The current Middle East war is not simply a geopolitical disruption. It is an energy shock intersecting with an industry already undergoing structural transformation. That intersection is what matters. The automotive industry is no longer defined by incremental improvements to internal combustion engines. It is shifting toward electrified, connected, software-defined mobility. When a shock of this magnitude hits during that transition, the outcome is not cyclical volatility. It is an acceleration of change.

The near-term effect is clear: rising costs, supply chain instability, and demand pressure. But the more important effect is structural. The war reinforces the economic and strategic logic of electrification, reshapes consumer behavior, and shifts competitive advantage toward those already aligned with the future. In that sense, it is a headwind for the industry, but a tailwind for its transformation.

Impact on Supply Chain: From Cost Shock to Structural Fragility

The first-order impact of the war is transmitted through energy. Disruption to flows through the Strait of Hormuz—one of the most critical arteries in the global oil system—drives fuel prices higher, increases freight costs, and introduces volatility into global logistics networks. This immediately affects the automotive supply chain because energy is embedded across every stage of production. It influences the cost of metals, plastics, chemicals, and components. It shapes manufacturing economics. It defines the cost of moving goods across regions.

In the early phase, the impact is primarily inflationary. Freight rates rise. War-risk insurance increases. Suppliers pass through higher input costs. Automotive OEMs and Tier suppliers face margin compression as they absorb or attempt to pass on these increases. At the same time, logistical delays begin to disrupt just-in-time systems that have been optimized for efficiency rather than resilience.

As the disruption persists, the nature of the risk shifts. It moves from cost to availability. Inventory buffers begin to erode, and the system becomes more sensitive to interruptions. This is where material exposure becomes critical.

Aluminum represents one of the most immediate vulnerabilities. It is a core material in modern vehicle architectures and increasingly important in electric vehicles due to its role in lightweighting and structural design. Disruptions in supply or transport translate directly into price increases and potential shortages, with limited substitution options in the short term.

Petrochemicals create a broader, more diffuse risk. Derived from oil and gas, they underpin a wide range of automotive components, from plastics and interiors to adhesives and coatings. Disruptions in LPG and naphtha flows constrain production of these materials, creating cost pressure that cascades through Tier 2 and Tier 3 suppliers. These effects are less visible but more pervasive.

A third layer of risk lies in industrial gases, particularly helium, which is critical for semiconductor manufacturing. While not an immediate bottleneck, constraints in this area introduce second-order risk to electronics supply chains, which are increasingly central to both traditional and electric vehicles.

The sequencing is predictable. First comes cost inflation. Then inventory depletion. If the disruption persists, production becomes constrained. The automotive supply chain, designed for global optimization, reveals its structural fragility under sustained energy disruption.

Impact on Consumer Demand: From Price Shock to Behavioral Shift

While the supply-side effects are immediate, the demand-side impact is more subtle and potentially more enduring. The key mechanism is fuel price.

When fuel prices rise sharply, operating cost becomes central to the consumer decision. This is not new. The oil shocks of the 1970s triggered a shift toward smaller, more fuel-efficient vehicles, reshaping market dynamics and enabling new entrants to gain share. What matters is not just the initial response, but the persistence of that response. Consumers internalize fuel-price shocks. They reassess long-term operating costs and adjust preferences in ways that can outlast the crisis itself.

What is different today is the nature of the substitute. In the past, consumers could only move within the internal combustion paradigm, choosing more efficient vehicles. Today, they can move away from oil dependence entirely. Hybrids, plug-in hybrids, and fully electric vehicles offer a structurally different value proposition.

As fuel prices rise, this substitution becomes economically compelling. Total cost of ownership becomes more visible. Electric vehicles, with lower and more stable operating costs, gain relative advantage. This is not driven by policy or ideology. It is driven by economics.

At the same time, the broader macro environment creates a countervailing effect. Higher energy costs and economic uncertainty suppress overall vehicle demand. Consumers delay purchases. Financing conditions tighten. The result is a divergence: total industry demand weakens, but the composition of demand shifts toward electrified and more efficient vehicles.

The key point is that the demand impact is not purely cyclical. It reflects a reassessment of energy risk. In that sense, the war does not just influence what consumers buy today. It influences how they think about mobility going forward.

Competitive Analysis: A Reordering of Advantage

The most important effect of the war is not cost or demand in isolation. It is the way those forces interact to reshape competitive dynamics.

The industry does not move uniformly. It rebalances.

The shift toward electrification strengthens the position of companies that are already aligned with that trajectory. China is the most prominent example. Its automotive industry has built scale in new energy vehicles, established leadership in battery production, and developed a high degree of vertical integration across key components of the EV stack. It is also increasingly export-oriented, with a growing share of production directed toward global markets.

In an environment where the economic case for electrification is reinforced, these advantages become more pronounced. Chinese automakers are able to offer competitive products at scale, supported by integrated supply chains that are more resilient to external disruption. The war does not create this advantage. It amplifies it.

By contrast, legacy automakers face a more complex challenge. Their exposure to internal combustion vehicles makes them vulnerable to shifts in consumer preference driven by fuel prices. At the same time, their transition to electric vehicles is often constrained by cost, profitability, and organizational complexity. Their supply chains are more fragmented, and their control over key components such as batteries and software is less developed.

This creates a dual pressure. They are exposed to the downside of the shock while being less fully positioned to capture the upside of the transition. The war effectively raises the cost of delay. It compresses the timeline over which legacy players must adapt, while reducing the margin for error.

It is important to recognize that not all electric vehicle players benefit equally. The same supply chain disruptions that affect the broader industry also impact EV production. The differentiator is not simply product mix, but capability. The winners are those who control the EV stack—batteries, software, and key components—and who operate at sufficient scale to manage cost and supply volatility.

This is not a universal uplift. It is a selective acceleration.

Shift in the Center of Gravity: From Mechanical to Electrical, from West to East

The combined effect of supply disruption, demand shift, and competitive rebalancing is a shift in the center of gravity of the automotive industry.

Historically, the industry was anchored in mechanical engineering, internal combustion technology, and Western and Japanese OEM dominance. That center is now moving along two dimensions.

The first is technological. The locus of value is shifting from mechanical systems to electrical architectures, software, and integrated energy systems. Control of batteries, power electronics, and software platforms is becoming more important than incremental improvements in engines and transmissions.

The second is geographic. As electrification becomes more central, the advantage shifts toward regions that have built scale and integration in these areas. China stands out in this regard, not only because of its production capacity, but because of its ecosystem approach—linking batteries, vehicles, software, and infrastructure.

The war accelerates both dimensions of this shift. By increasing the cost and volatility associated with oil dependence, it strengthens the case for electrification. By favoring integrated, scalable systems, it advantages those regions and companies that have already invested in that model.

This does not mean that Western or Japanese automakers are displaced in the near term. But it does mean that the trajectory of competitive power is changing, and that change is being pulled forward.

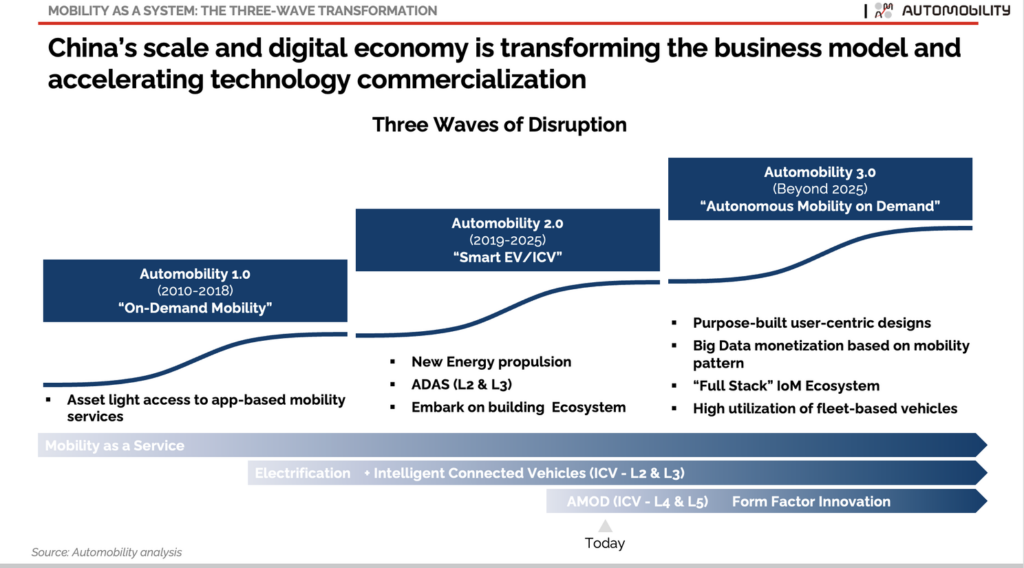

Automobility Lens: Accelerating the Second Wave

Viewed through the Automobility framework, the impact of the war is uneven across the three waves.

Automobility 1.0, defined by shared mobility services, experiences mixed effects. Higher fuel costs increase operating expenses for fleets, while economic uncertainty may reduce discretionary usage. There may be some substitution from ownership to usage, but this is not the dominant dynamic.

Automobility 2.0, centered on electric and connected vehicles, is the primary beneficiary. The war reinforces the economic logic of this phase by increasing the cost of oil-dependent mobility and strengthening the relative value proposition of electrification. It also highlights the importance of system-level integration, including batteries, software, and energy management.

Automobility 3.0, focused on autonomous mobility, is less directly impacted in the near term. While higher energy costs support the long-term case for optimized, fleet-based mobility systems, the capital intensity and technological complexity of this phase mean that progress may be constrained in the short term by economic uncertainty and supply chain disruption.

The net effect is that the war accelerates the second wave while leaving the third largely intact but deferred.

Conclusion: Compression of Time, Expansion of Divide

The current Middle East war does not change the direction of the automotive industry. That direction was already set. What it does is compress the timeline and sharpen the competitive divide.

In the near term, the industry faces clear headwinds. Costs rise. Supply chains are strained. Demand weakens. But beneath these pressures, a more important shift is taking place. Consumer preferences are evolving. The economic case for electrification is strengthening. Competitive advantage is moving toward those who control the technologies and systems that define the next phase of mobility.

Weak players become more exposed. Strong players extend their advantage. The center of gravity continues to shift.

The simplest way to frame it is this:

The industry slows down. The transition speeds up.

And that is where the real impact lies.

About the Author

Bill Russo is the Founder and CEO of Automobility Ltd, and is currently serving as the Chairman of the Automotive Committee at the The American Chamber of Commerce in Shanghai (AmCham Shanghai). His over 40 years of experience includes 15 years as an automotive executive with Chrysler, including 22 years of experience in China and Asia. He has also worked nearly 12 years in the electronics and information technology industries with IBM and Harman. He has worked as an advisor and consultant for numerous multinational and local Chinese firms in the formulation and implementation of their global market and product strategies. Bill is a contributing author to the bookSelling to China: Stories of Success, Failure, and Constant Change (2023), where he describes how China has become the most commercially innovative place to do business in the world’s auto industry – and why those hoping to compete globally must continue to be in the market.

Contact Bill by email at bill.russo@automobility.io

About Automobility

Automobility Limited is global Strategy & Investment Advisory firm based in Shanghai that is focused on helping its clients to Build and Profit from the Future of Mobility. We help our clients address and solve their toughest business and management issues that arise in midst of fast changing, complicated and ambiguous operating environment. We commit to helping our clients to not only “design” the solutions but also raise or deploy capital and assist in implementation, often together with our clients.

Contact us by email at info@automobility.io

No Comments