21 Mar State of China’s Auto Market – February 2026

Written by Bill Russo, Founder & CEO of Automobility Ltd.

Recognized for the 7th Time

I’m deeply honored to receive the 2025 Contribution Award from The American Chamber of Commerce in Shanghai. Being acknowledged for the 7th time during my tenure as Chair of the Automotive Committee is something I take great pride in.

This recognition reflects not just individual effort, but the collective work of an outstanding committee, engaged member companies, my Automobility team, and a broader automotive community committed to constructive dialogue and collaboration. China’s automotive and mobility landscape continues to evolve at extraordinary speed, and creating a platform for informed, open exchange has never been more important.

My sincere thanks to AmCham Shanghai for its continued trust and leadership, and to all the colleagues and partners who have contributed along the way.

The work continues. 🙏🚗🌏

January Results

-

January opened weak as subsidy roll-off pulled demand into late 2025, driving a -14.5% YoY decline and exposing policy-sensitive segments. -

NEVs remain the structural growth engine, but January’s reset pushed NEV share down to ~39–40%, with volumes falling faster than ICE. -

The halving of NEV purchase tax exemptions and tighter trade-in rules triggered disproportionate pressure on price-sensitive domestic brands. -

VW reclaimed the No.1 PV position as BYD volumes corrected sharply, underscoring the month’s ranking volatility. -

NEV mix rotated upmarket with premium and technology-led players (HIMA, Xiaomi) sustaining momentum despite the broader slowdown. -

Tesla recorded its strongest export month, using Giga Shanghai as a swing capacity base to offset weak domestic demand. -

Calendar effects (later Lunar New Year) inflated January selling days, increasing downside risk for February volumes. -

Despite near-term turbulence, total volumes remain structurally above the post-2017 down-cycle baseline, supported by a permanently higher export share and electrified mix.

A Weak Opening

In China, 2026 is the Year of the Horse—symbolizing speed, strength, and forward momentum. However, the opening months of the China auto market require careful interpretation. Year-over-year comparisons in January and February are inherently distorted by Lunar New Year timing, which falls more than two weeks later in 2026 than in 2025, affecting selling days, production schedules, logistics flows, and dealer traffic nationwide.

In addition, there was a clear pull-ahead effect into late 2025 as consumers accelerated purchases ahead of expiring incentives and in anticipation of reduced subsidy intensity in 2026. As a result, early-year softness reflects a combination of calendar distortion and policy normalization rather than a clean read on underlying demand. A more reliable assessment of China’s market trajectory will emerge after first-quarter effects have fully washed through the system.

China Auto Adjusts After Incentive Pull-Forward

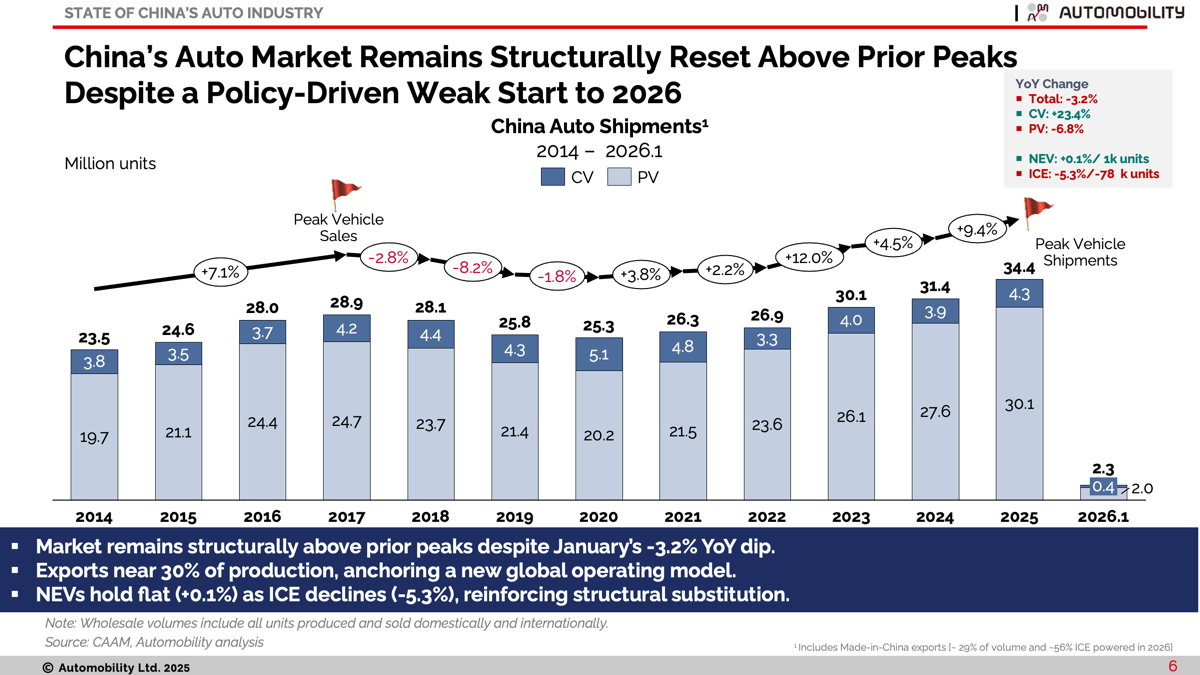

China’s auto market exited 2025 at a new structural high, with total vehicle shipments (domestic + exports) rising ~9.4% year over year to a record ~34.4 million units, decisively surpassing the prior 2017 peak and confirming a reset in the industry’s operating baseline.

However, January 2026 opened softer, with total shipments down -3.2% YoY, reflecting subsidy roll-off and Lunar New Year timing effects rather than a break in structural momentum.

Growth in 2025 was driven overwhelmingly by electrification. NEV shipments increased by ~3.6 million units (+28% YoY), becoming the market’s clear marginal growth engine. In contrast, ICE volumes declined modestly (~-4% YoY)—a meaningful contraction, but insufficient to offset overall expansion as exports now account for nearly 30% of total production, reinforcing scale.

January shipment dynamics show a temporary pause rather than structural reversal: NEVs held roughly flat year over year (+0.1%), while ICE volumes declined further (-5.3%), contributing to the overall softness.

Taken together, the data confirms a durable shift in China’s auto market structure: exports anchor volume, electrification defines long-term direction, and early-2026 weakness reflects policy and calendar effects—not a reset of the higher structural baseline established in 2025.

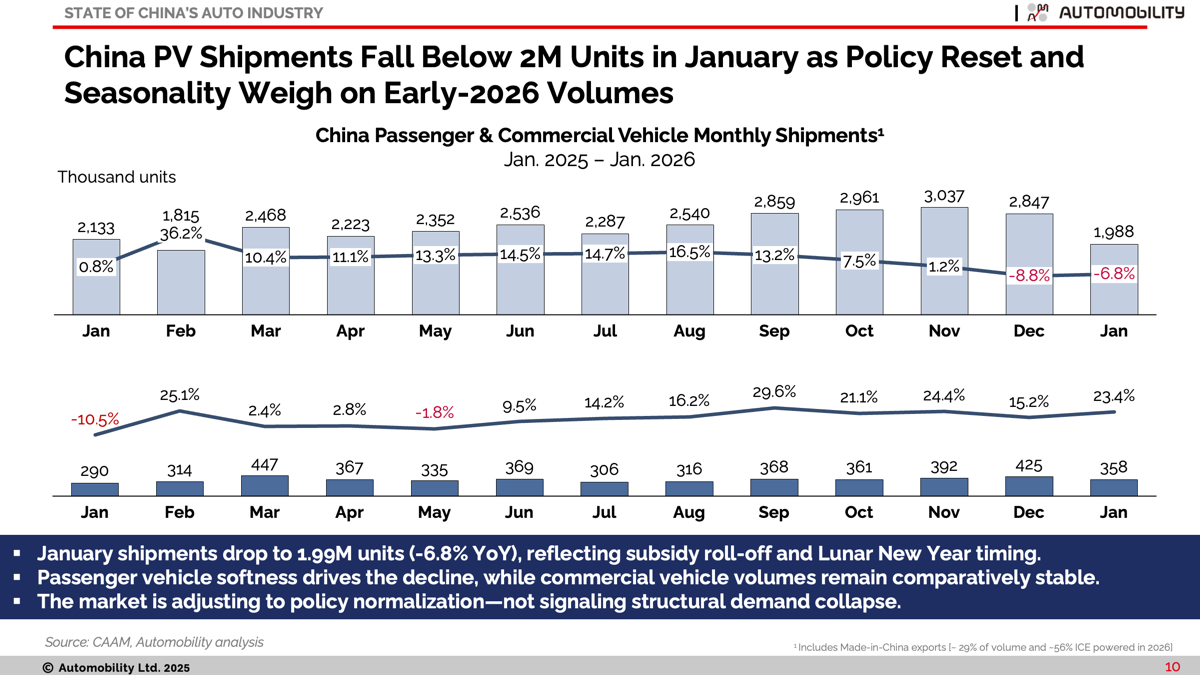

Monthly shipments peaked above 3.4 million units in late 2025 but fell to 2.3 million units in January (-3.2% YoY), reflecting subsidy roll-off and Lunar New Year timing effects. While this marks a clear step down from Q4 levels, volumes remain consistent with seasonal patterns rather than signaling a structural break in demand.

The transition into 2026 highlights a shift from late-year volume pull-forward to policy-driven normalization. January passenger vehicle softness accounts for the bulk of the decline, while commercial vehicle volumes were comparatively strong. The data suggests the market is adjusting to incentive changes and calendar distortion.

Taken together, the year-end and January data point to a policy- and calendar-driven reset rather than a structural reversal in China’s auto market. Late-2025 volumes were supported by incentive pull-forward, pushing shipments to elevated levels before normalization set in. The January decline—particularly in passenger vehicles—reflects subsidy roll-off and Lunar New Year timing distortion more than a deterioration in underlying demand. The market has shifted from acceleration to adjustment, with early-2026 softness representing payback from Q4 strength rather than a break in China’s higher, export-anchored structural baseline.

Exports Anchor Scale as Electrification Redefines Growth

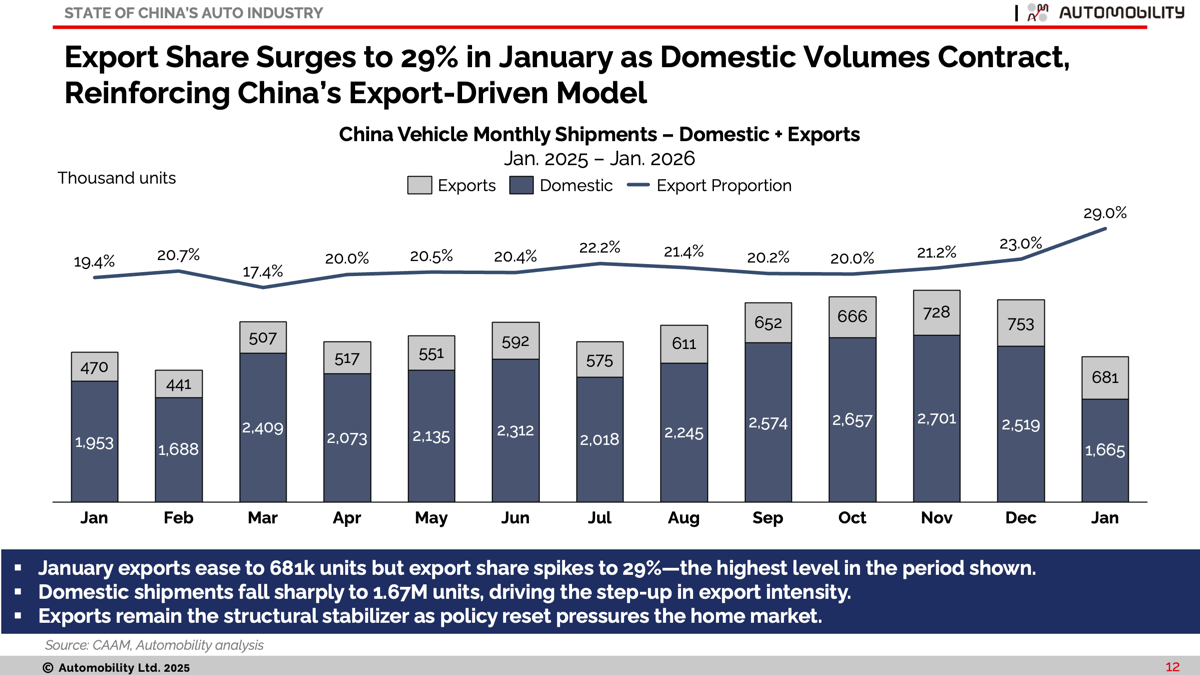

Exports continue to provide structural ballast for China’s auto industry. While January export volumes eased to 681,000 units, their importance increased meaningfully: exports accounted for 29% of total vehicle shipments, the highest share in the period shown. The rise in export intensity was driven primarily by a sharp contraction in domestic volumes, underscoring how overseas demand is now cushioning policy-driven softness at home. What was once a cyclical release valve has become a foundational pillar of China’s automotive operating model—anchoring scale, sustaining utilization, and reinforcing the market’s export-led structural reset.

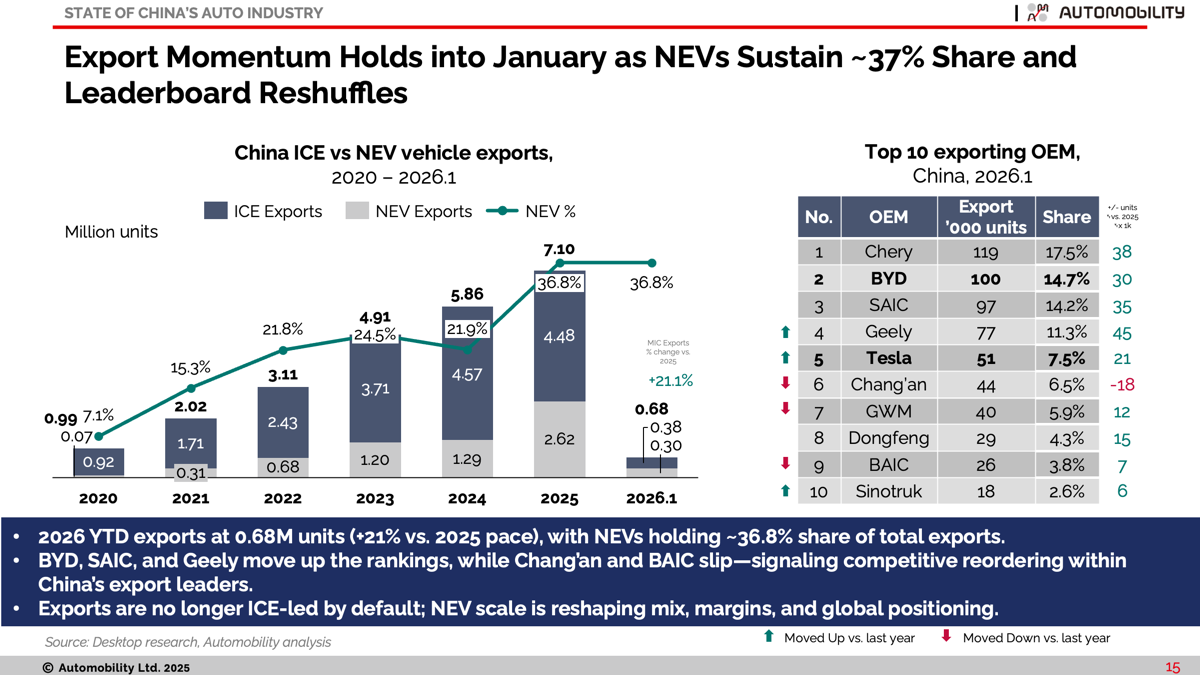

China exited 2025 with record vehicle exports of approximately 7.1 million units, firmly establishing exports as a structural growth pillar rather than a cyclical outlet. That momentum has carried into early 2026: January exports reached 0.68 million units (+21% vs. 2025 pace), underscoring continued external demand even as domestic volumes softened.

NEVs now account for roughly 36–37% of total exports, reinforcing that China’s export engine is no longer ICE-led by default. Electrified vehicles are increasingly defining mix, margins, and global positioning, while shifts in the top exporter rankings signal intensifying competition among China’s leading OEMs in overseas markets.

Structural Shift, Tactical Reset

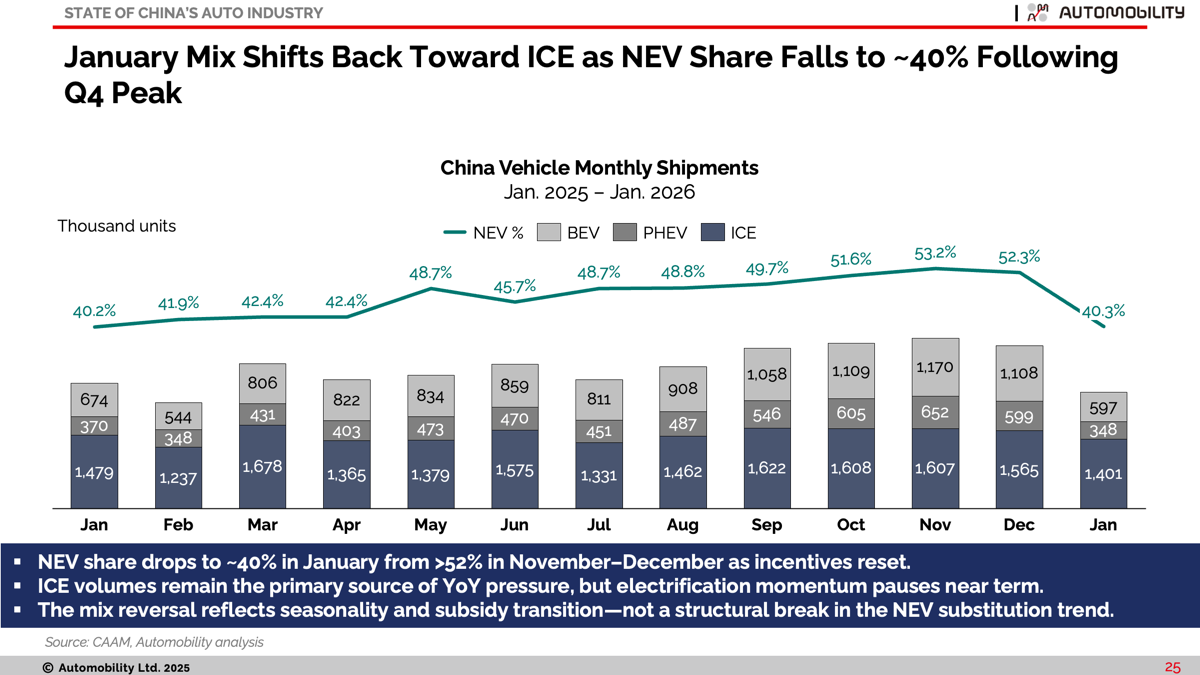

China closed 2025 with record NEV shipments of ~16.5 million units, cementing electrification as the market’s primary growth engine. By year-end, NEV share had climbed above 52%, reflecting ICE-led softness and record BEV/PHEV output in Q4.

However, January opened with a clear mix reset. NEV share fell back to ~40% as incentives stepped down and seasonal effects distorted volumes. Both BEV and PHEV shipments declined from Q4 peaks, while ICE volumes increased in relative mix terms.

The implication is tactical, not structural. 2025 confirmed electrification as the dominant trajectory, but January shows that subsidy timing still influences monthly mix. ICE remains the adjustment variable over the cycle, while NEVs continue to define the long-term direction of China’s auto market.

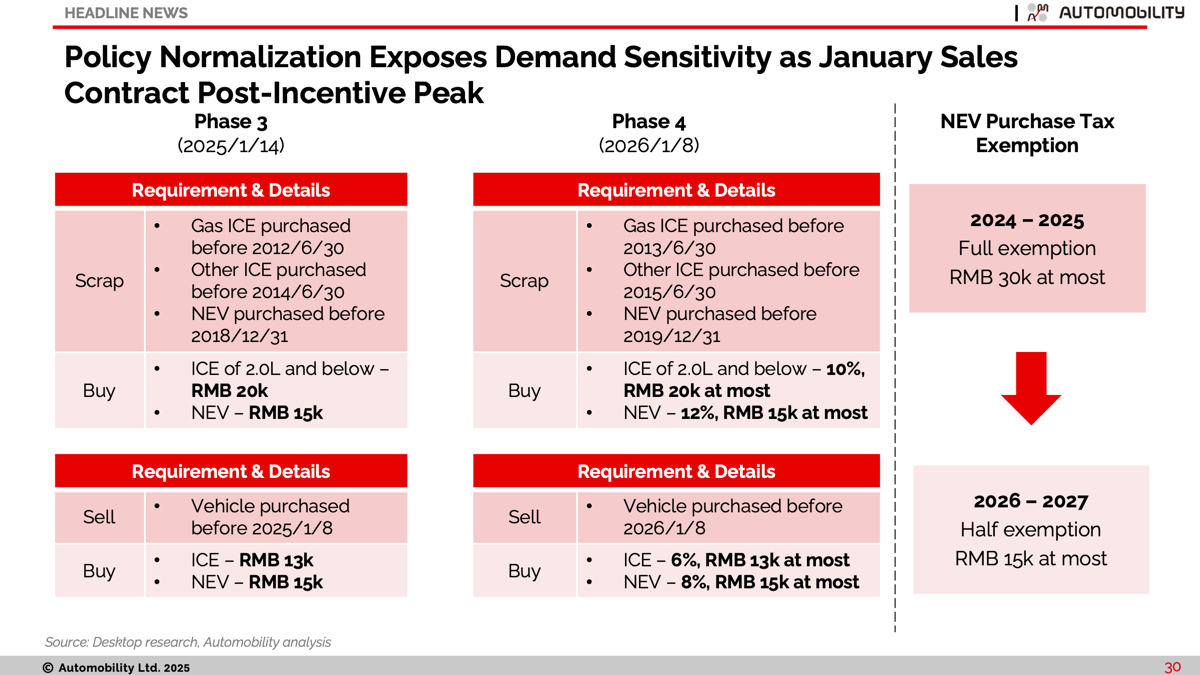

The shift from Phase 3 to Phase 4 materially changes the economics at the point of sale for retail passenger vehicle consumers. The NEV purchase tax exemption has been halved in 2026 (from a full exemption capped at RMB 30,000 to RMB 15,000), effectively raising transaction prices for many EV buyers. At the same time, trade-in requirements have tightened, narrowing eligibility windows and reducing the intensity of subsidy support.

The predictable outcome was a pull-forward of demand into late 2025, followed by a payback effect in January. Consumers who were incentive-sensitive accelerated purchases ahead of expiry, leaving a softer opening to 2026 once subsidies stepped down.

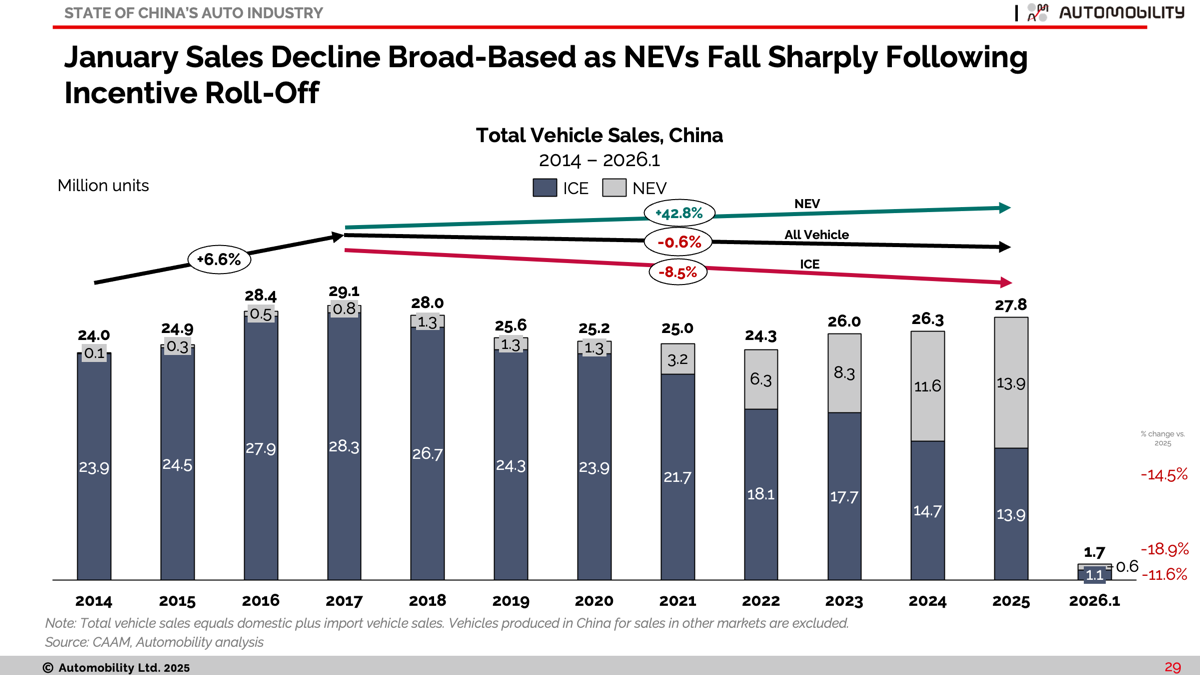

China’s domestic auto market rebounded in 2025, with total vehicle sales reaching 27.8 million units (+~4–5% YoY). But January 2026 opened sharply weaker, with sales falling to 1.7 million units (-14.5% YoY) following incentive roll-off.

The 2025 recovery was entirely mix-driven. NEV sales surged (+~43% YoY) while ICE volumes declined (~-8–9%), meaning electrification accounted for all net growth. By year-end, NEVs and ICE were roughly balanced in volume terms.

January tells a different short-term story. NEV sales fell -18.9% YoY, declining faster than ICE (-11.6%), reflecting policy normalization and pull-forward effects rather than structural reversal.

The broader shift remains intact: China’s growth is defined by mix transformation, not volume recovery to prior peaks. ICE is the adjustment variable, and long-term scale depends on electrification—even if early-2026 volatility temporarily obscures that trajectory.

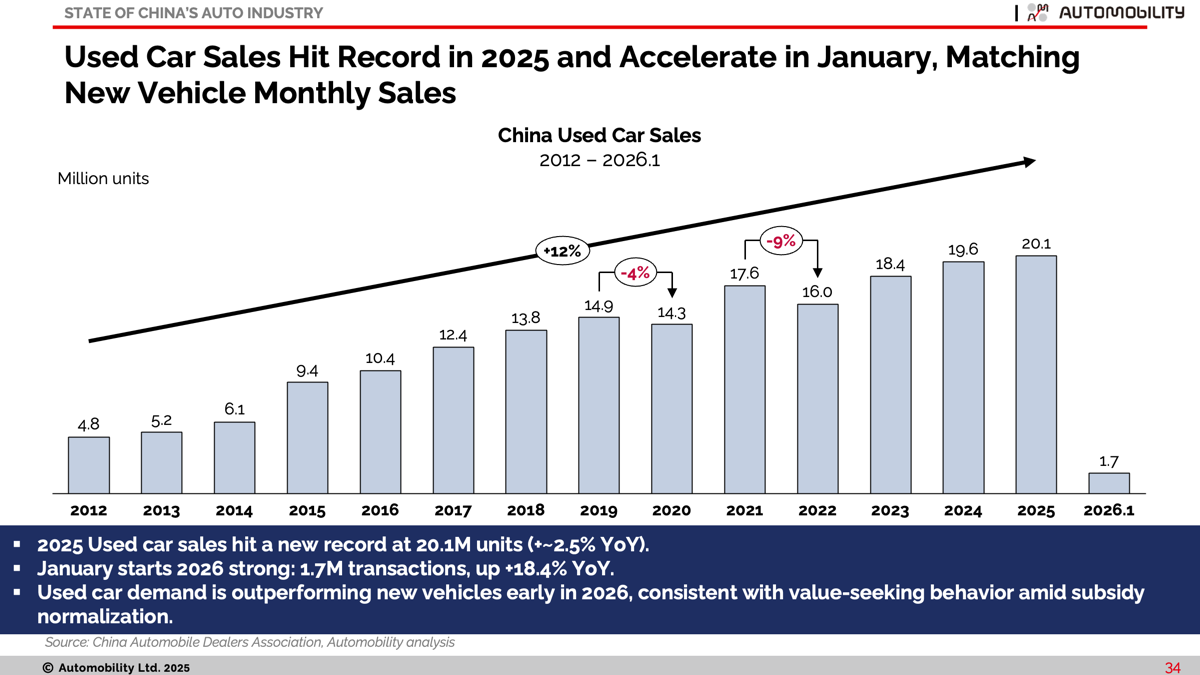

It is notable that used car sales rose +18.4% YoY in January, sharply outperforming the new vehicle market in what was otherwise a weak month for auto demand. This divergence suggests a migration of price-sensitive consumers from new to used vehicles, particularly following the step-down in new car incentives. As purchase tax benefits were halved and trade-in requirements tightened, affordability gaps widened—redirecting budget-constrained buyers toward the secondary market.

In this context, used car sales strength is less about cyclical acceleration and more about substitution behavior driven by policy normalization. Early-2026 demand has not disappeared; it has partially shifted channels.

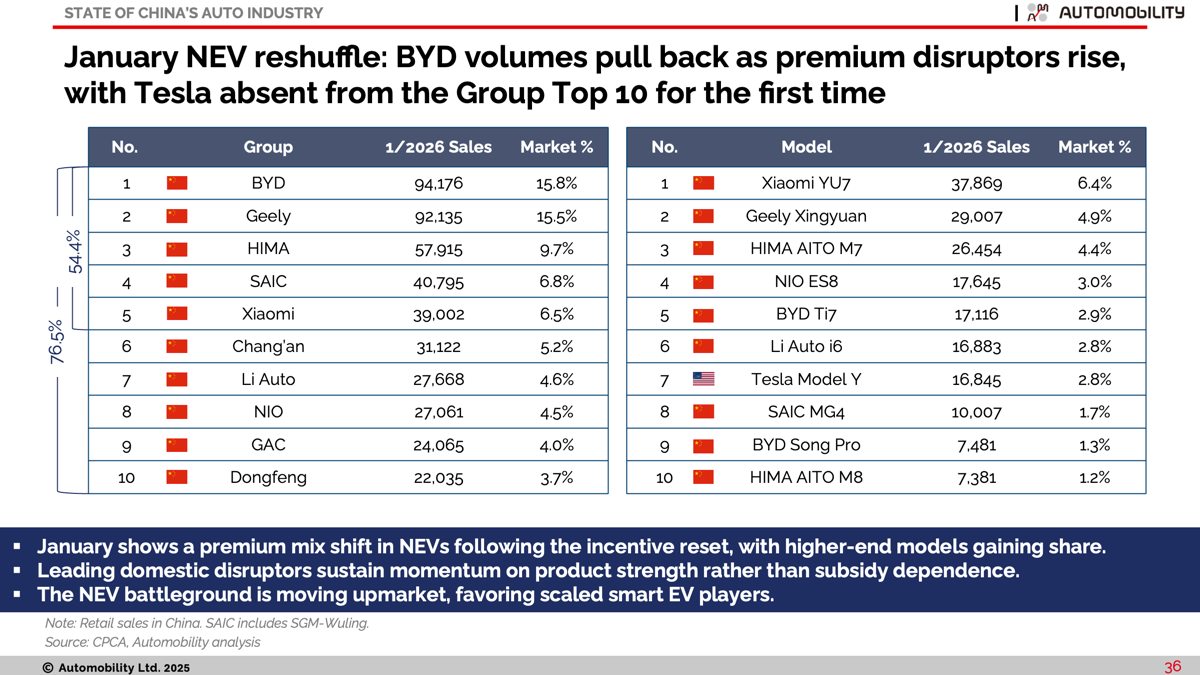

Upmarket Momentum Builds as Mass-Market EVs Stall

January’s Top 10 rankings reflect a clear policy-driven reshuffle. BYD retained the No.1 position but with a notable share pullback, highlighting its greater exposure to price-sensitive segments following the subsidy reset. The mix rotated decisively upmarket, with premium and technology-forward players such as HIMA and Xiaomi gaining relative ground as higher-income buyers proved less incentive-dependent. Tesla’s absence from the Group Top 10 underscores the volatility created by its export pivot and softer domestic deliveries.

At the nameplate level, the disappearance of entry models such as Wuling Hongguang Mini EV and BYD Seagull reinforces the impact of halving of purchase tax benefits and tighter trade-in requirements which disproportionately impacts ultra-low-priced vehicles, compressing volumes at the bottom of the market while resilience shifted toward higher-end, brand-driven demand.

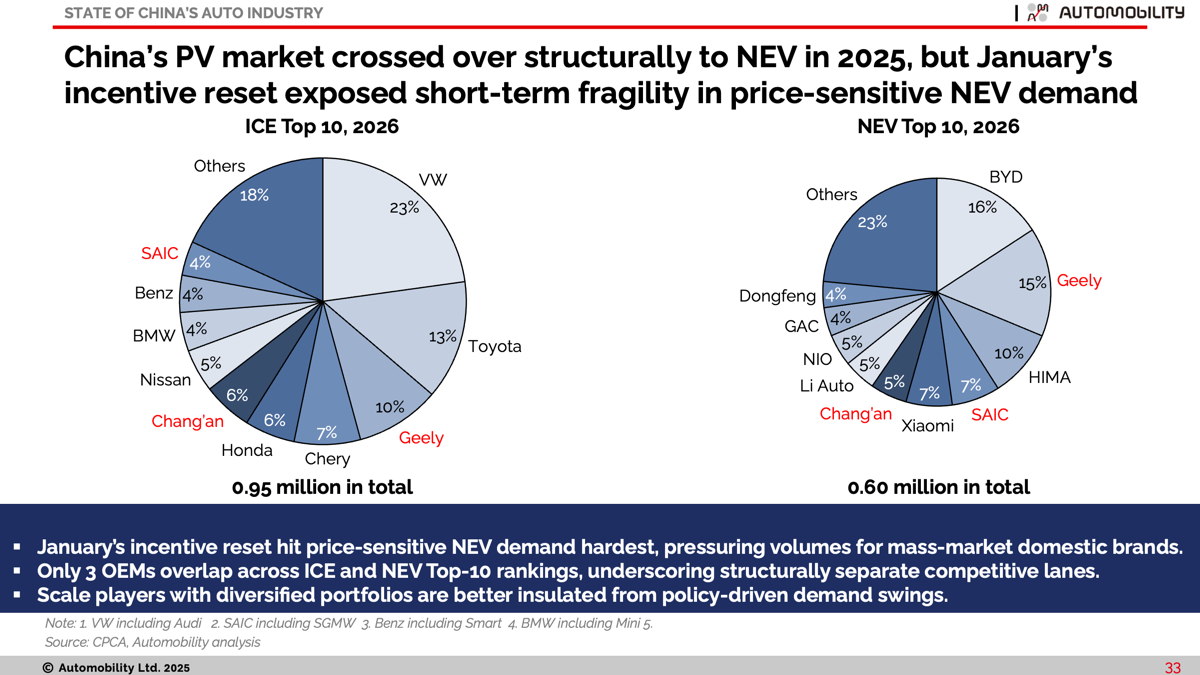

China’s passenger vehicle market structurally crossed over to NEV leadership in 2025, but January’s incentive reset exposed clear short-term fragility in price-sensitive demand. The halving of NEV purchase tax exemptions and tighter trade-in requirements disproportionately impacted mass-market domestic brands, driving a pullback in NEV share and sharper corrections at the lower end of the market.

The Top 10 comparison highlights a deepening bifurcation between ICE and NEV competitive lanes, with only three OEMs overlapping across both rankings. Scale and portfolio diversification are emerging as key shock absorbers, while pure-play, price-sensitive segments remain more vulnerable to policy-driven volatility.

Note that only 3 brands (highlighted in red) are ranked as top 10 players for both ICE and NEV, and they are all Chinese: Geely, Chang’an and SAIC.

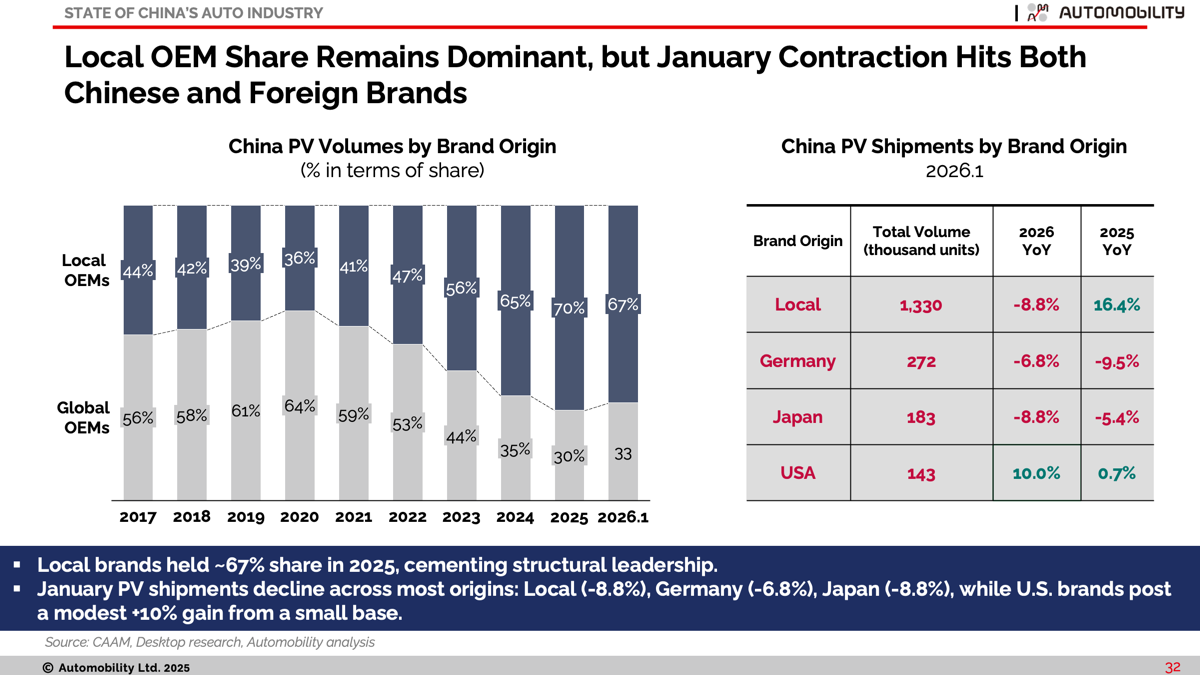

Local Brand Dominance Intact, but Incentive Normalization Triggers Tactical Share Pressure

Local brands retained structural dominance at 67% share of PV sales, but January data shows a modest near-term reduction. Local OEM volumes declined -8.8% YoY, slightly more pronounced than Germany (-6.8%) and in line with Japan (-8.8%), while U.S. brands posted a small gain from a low base.

The January share compression for Chinese brands likely reflects subsidy step-down effects, which disproportionately impact the price-sensitive mass-market segments where local OEMs are most concentrated. With NEV purchase tax benefits halved and trade-in requirements tightened, incentive elasticity appears higher among domestic brands’ core customers.

Importantly, this looks tactical rather than structural. The broader competitive reset in favor of Chinese OEMs remains intact, but January illustrates how policy normalization can temporarily pressure share in segments most exposed to subsidy intensity.

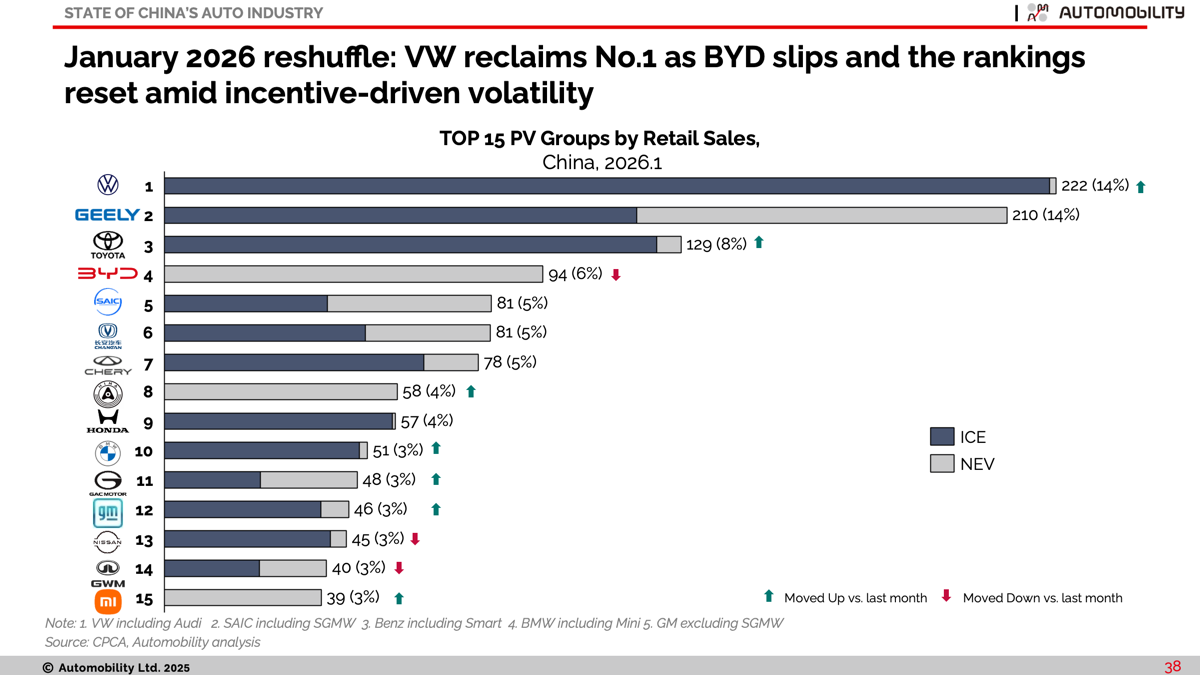

January’s Top 15 total PV sales rankings illustrate how sharply the incentive reset reshuffled the competitive order. VW reclaimed the No.1 position, benefiting from relative ICE stability and less exposure to subsidy-sensitive segments, while BYD slipped amid a correction in price-sensitive NEV volumes. Geely held firm near the top, reflecting stronger balance across ICE and NEV portfolios. The month reinforces that one data point during a policy transition does not define a new structural trend, but it does expose underlying demand elasticity: brands skewed toward mass-market electrification saw sharper volatility, while diversified players with scale and ICE carryover proved more insulated. The result is a temporary reset in rankings layered on top of a still-intact structural shift toward electrification.

Conclusion: January Marks a Policy-Driven Reset

The incentive step-down pulled forward late-2025 demand and exposed elasticity in price-sensitive NEV segments, driving a temporary drop in NEV share and sharp ranking volatility. Premium and technology-led players proved more resilient, exports played a growing shock-absorber role, and diversified OEMs with ICE carryover outperformed pure-play mass-market EV names. The underlying crossover to electrification remains intact, but the month underscored how dependent near-term volumes still are on policy calibration.

Looking ahead in 2026, the key variables to monitor are February follow-through after calendar impact of the later Chinese New year, the stability of NEV mix and share as incentives normalize, and whether premiumization continues to offset weakness at the entry level. Export intensity will be critical in cushioning domestic softness, while competitive pressure and regulatory tightening will test margin discipline across the value chain. The central question is not whether electrification continues—it will—but who captures the profit pool in a more volatile, less subsidy-supported growth phase.

AmCham Shanghai State of China Auto Market Monthly Webinar [February 24]

Join us on Tuesday, February 24, from 9:00 am – 10:15 am China time for the monthly AmCham Shanghai State of China Auto Market Monthly Webinar, where we will review the latest market results through January 2025 and highlight recent news from the world’s largest and most progressive automotive market.

Webinar | State of China Auto Market Monthly Briefing (February) | AmCham Shanghai

AUTOMOBILITY FRAMEWORK AUDIO INTERVIEW SERIES

As China’s auto industry enters a decisive phase of global influence, it is increasingly evident that what is underway is not a simple EV transition, but a multi-wave restructuring of how mobility is conceived, industrialized, and scaled.

To frame this shift, I am recording a three-part audio interview series with Ron Hesse from GlobalAutoIndustry.com that explores the Automobility 1.0–2.0–3.0 framework—from the move away from vehicle ownership toward usage-based mobility, through today’s connected, electric, and intelligent vehicle era, and ultimately toward autonomous, AI-driven mobility platforms.

Links to the first two interviews—Automobility 1.0 and Automobility 2.0—are provided below:

Automobility 1.0: The Shift from Ownership to Usage – A China Perspective

Automobility 2.0: Connected, Electric & Intelligent – A China Perspective

I will share a link to the third and final interview in the series on Automobility 3.0 when it is released in March, completing the arc of how China is reshaping the future of the global automotive industry. This topic is also explored in our article, The Third Wave of Disruption: Autonomous Mobility on Demand:

The Third Wave of Disruption: Autonomous Mobility on Demand

AUTOMOBILITY IN THE MEDIA

China bans Tesla style door handles

Financial Times, February 3, 2026

🇨🇳🚗 China bans hidden EV door handles — a signal of where EV regulation is heading

China has become the first major market to ban Tesla-style hidden / flush door handles, citing safety risks during accidents and power failures. The new rule, effective 2027, requires:

🔹 Clearly visible exterior door handles

🔹 Mechanical release mechanisms on every door

🔹 Redundancy beyond purely electronic systems

While flush handles became a design hallmark of modern EVs, real-world incidents have exposed their limitations in emergency scenarios.

💬 My comment in the Financial Times:

“The new rule would require changes to some EV models sold in China but not a ‘clean-sheet’ redesign. Many original equipment manufacturers already engineer alternative handle solutions for export markets with different regulations. The incremental cost impact per vehicle is likely modest — measured in tens of dollars rather than hundreds — especially for high-volume platforms.”

🔍 Why this matters:

This move reflects a broader regulatory shift as EVs transition from early adopters to the mass market. China is signaling that safety, resilience, and standardization now take precedence over design novelty.

Expect implications for:

⚙️ Global platform architectures

🌍 Homologation and export strategies

📐 The balance between form, function, and regulation in next-gen EV design

China bans hidden EV door handles in world-first safety rule

Bloomberg News, February 2, 2026

🚗⚡ China just rewrote the global EV safety playbook.

China has become the first country to ban concealed EV door handles, requiring clear mechanical releases inside and outside the vehicle. The rule takes effect in 2027, following fatal accidents where power failures prevented doors from opening.

This isn’t just a design tweak — it’s a signal shift.

As I shared with Bloomberg:

“China is shifting from being just the largest EV market to being a rule-setter for how new vehicle technologies are regulated.”

With China’s scale and export influence, these standards are likely to travel globally, reshaping vehicle design choices for both Chinese and foreign automakers — and reinforcing China’s growing role in setting the rules for Automobility 2.0.

Safety, not sleekness, is becoming the new baseline.

BYD burns profit chasing global dominance over Tesla

Rest of World, January 13, 2026

📉 Scale before profit — by design.

A timely piece from Rest of World looks at BYD’s deliberate choice to sacrifice near-term profitability in pursuit of global scale, as it accelerates overseas expansion and R&D investment.

As I noted in the article:

“BYD is now in a scale-before-profit phase internationally. This inevitably weighs on margins.”

This is not a failure of execution — it’s a strategic tradeoff. China’s leading EV players understand that global dominance is won by building volume, learning curves, and localized ecosystems first, with profitability following later. We’ve seen this playbook before in China’s domestic market — and now it’s being applied globally.

The real question isn’t whether margins are under pressure today. It’s whether BYD (and its peers) can successfully localize manufacturing, supply chains, and cost structures across diverse markets without eroding quality or brand trust. If they do, long-term global profitability becomes very real.

China wants more homegrown chips in its cars. The hard part isn’t geopolitics

Channel News Asia. January 23, 2026

China’s push to localize automotive semiconductors is often framed as a geopolitical story — but in reality, the hardest problems are technical, architectural, and ecosystem-driven.

This Channel News Asia analysis does a solid job unpacking where localization is actually happening (mature control chips) — and where it remains difficult (high-end compute for ADAS, autonomous driving, and digital cockpits).

As I noted in the piece:

“Redesigning electronic control units or software stacks around new chips can introduce cascading complexity, particularly for platforms already in production.”

The takeaway:

🚗 Chip localization in China is progressing — but unevenly

⚙️ The real bottlenecks are validation, integration, tooling, and supply stability

🌍 As Chinese automakers globalize, dual-supply strategies will remain the norm

This is less about ideology — and more about systems engineering, risk management, and time.

New Rules Could Force Tesla to Redesign Its Door Handles. That’s Harder Than It Sounds

Wired, October 13

🚪 China Sets the Standard — Again 🇨🇳⚙️

Tesla’s retractable door handles once symbolized futuristic design — sleek, digital, and aerodynamic. But as WIRED reports, they’ve now become the subject of safety investigations in the U.S. and lawsuits over trapped passengers.

Now, China is stepping in with new rules requiring mechanical door handles operable without tools — a move that could reshape global car design.

“This is a classic example of China setting the guardrails early: protecting consumers while quietly shaping global design standards.”

— Bill Russo, CEO of Automobility Ltd, quoted in WIRED

From EV batteries to autonomous driving and now even door handles, China is again leading not just in speed of innovation — but in defining the rules of the game.

AUTO INSIDER PODCAST

Auto Insider Podcast: Episodes #1 – #5

🎙️ Catch Up on the latest Episodes of the Auto Insider Podcast hosted by Bill Russo. Insights from the front lines of China’s mobility transformation — where speed, scale, and strategy are redefining global competition.

🌏 Episode #5: Safety Without Borders: How Autoliv Drives Scaled Collaboration in the Smart Mobility Era with Sng Yih, President, Autoliv China

🌏 Episode #4: Leapmotor’s Global Leap — A New Paradigm for Global EV Collaboration with Michael Wu, Co-President, Leapmotor

🚗 Episode #3: Competing at China Speed: A Tier-1 Perspective from Magna with Zhen Wu, President of Magna China

🦋 Episode #2: The Butterfly Effect—How China’s Auto Shift is Reshaping the World with Dr. Xiaozhi Liu, Founder and CEO of ASL Automotive, Former CEO of Fuyao Glass

🔧 Episode #1: Smart EVs and the Smart Tier 0.5 Supply Chain with Jack Cheng , Co-Founder of NIO and CEO of M-Mobility

We’re just getting started — more conversations coming soon with the visionaries shaping the future of mobility.

About Bill Russo

Bill is a contributing author to the book Selling to China: Stories of Success, Failure, and Constant Change (2023), where he describes how China has become the most commercially innovative place to do business in the world’s auto industry – and why those hoping to compete globally must continue to be in the market.

About Automobility

Contact us by email at info@automobility.io

PLEASE NOTE: The information and analysis shared in this newsletter, including the charts and style of materials presented, is the intellectual property of Automobility Ltd. While we share it as a way to serve our existing and new clients, it is not to be used without our express consent and then only with attribution. Any publication, reproduction or other use of this material without the express written consent of Automobility Ltd is prohibited.

Sorry, the comment form is closed at this time.